Review date: May 20, 2024

All numbers on charts are in thousands USD, except when stated otherwise.

Verdict:

We can’t recommend Block. They improved profitability by controlling costs and via Bitcoin appreciation. But it’s a growth company and the growth is slowing.

Pros:

- improving operating margin;

- above average gross profit growth from the Subscription and Bitcoin segments.

Cons:

- 2024 is expected to be the third year of slowing growth;

- net profit is volatile, with half of earnings in Q1 2024 coming from the change in Bitcoin price;

- significant share-based compensation.

Important to know

It is hard to compare Block’s sales with peers because of the accounting policy for Bitcoin revenue. The company considers the value of all Bitcoins sold to customers as revenue.

And the cost of these Bitcoins – as the cost of goods sold. As a result, the Bitcoin segment produced 45.8% of total revenue, but only 3.8% of gross profit during Q1 2024. This makes gross profit the key metric for comparison.

Dr. Michael Burry’s hedge fund increased its stake in Block by 80% during Q1 2024, making it his sixth biggest holding. Our best guess is he saw significantly improving earnings as a possible catalyst for higher share price. Note that he could have sold his stake already.

On May 1, 2024 NBC News issued an article about Block’s potential examination by federal prosecutors. Allegedly Square processed thousands of transactions involving countries subject to economic sanctions, and Block processed multiple cryptocurrency transactions for terrorist groups.

This increases the risk of fines and potentially the need for costlier know-your-client policies.

CEO comments on this news are on page 2 of the prepared remarks for the Q1 2024 earnings call.

On March 23, 2023, Hindenburg Research, the famous short-selling research firm, issued a report on Block, alleging the company inflated user metrics and facilitated “frictionless” fraud.

Hindenburg’s report.

Block’s first response.

Block’s detailed statement.

Hindenburg’s response to the Block’s statement.

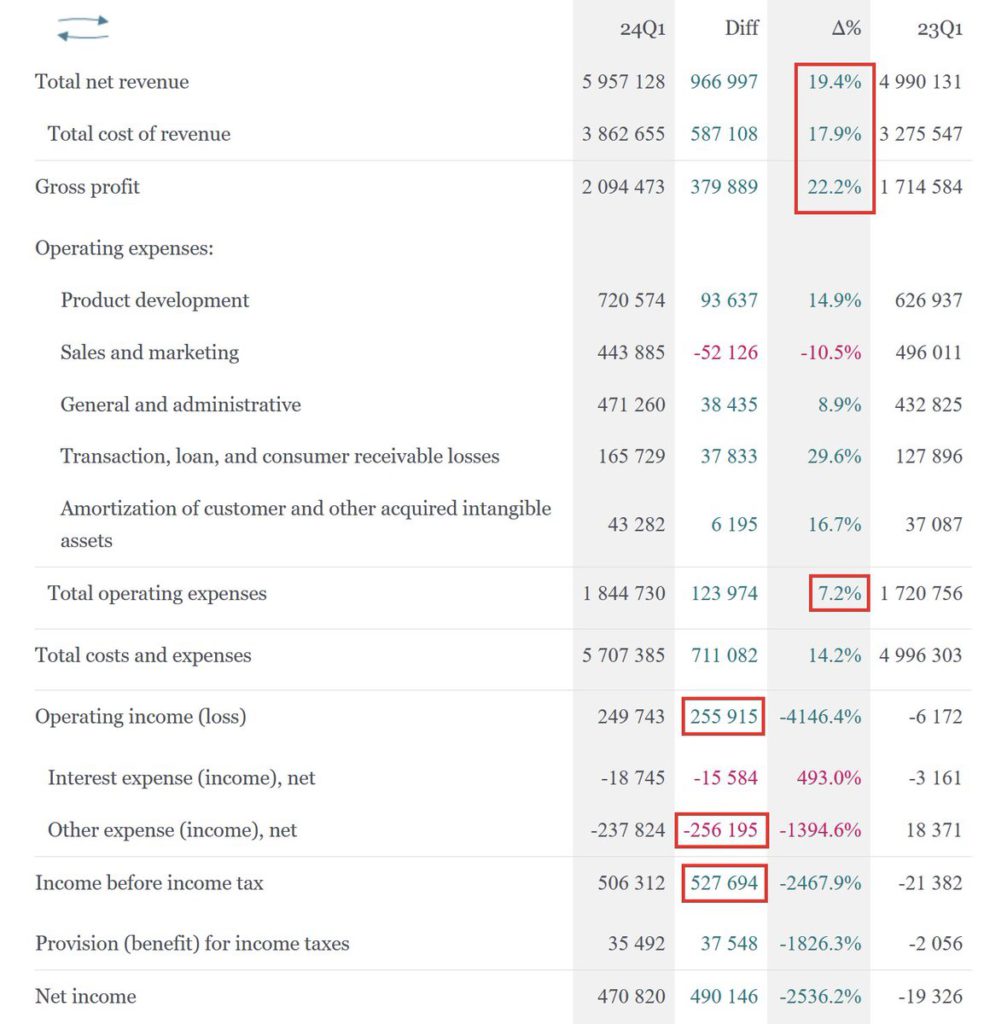

Profit and loss

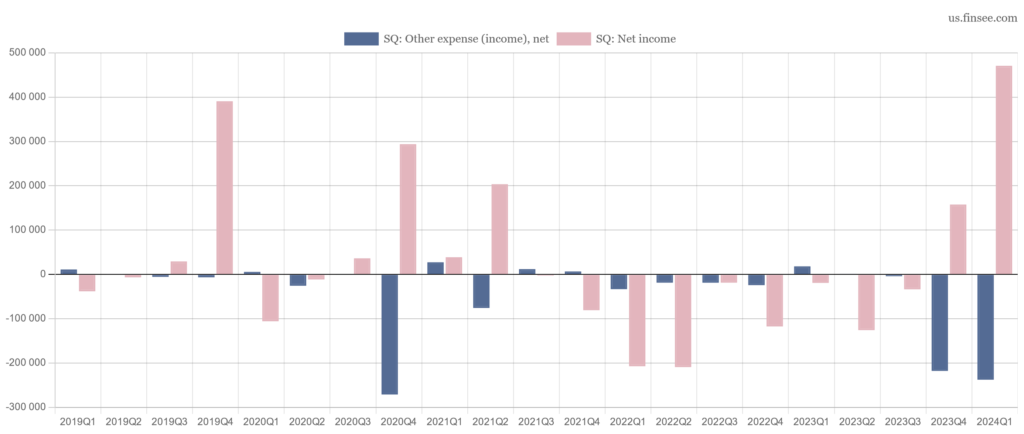

Block posted a significant profit for Q1 2024. One-half of it comes from the remeasurement of Bitcoin investment (other expense). Second half – from controlling marketing and administrative spending.

Comparison between Q1 2024 and Q1 2023 Profit and loss:

Bitcoin price is highly volatile, bringing significant upside to the earnings in good periods (2020 Q4, 2023 Q4, 2024 Q1). But how long will this trend last?

When Other expense (Bitcoin remeasurement is here) goes negative, the company receives income.

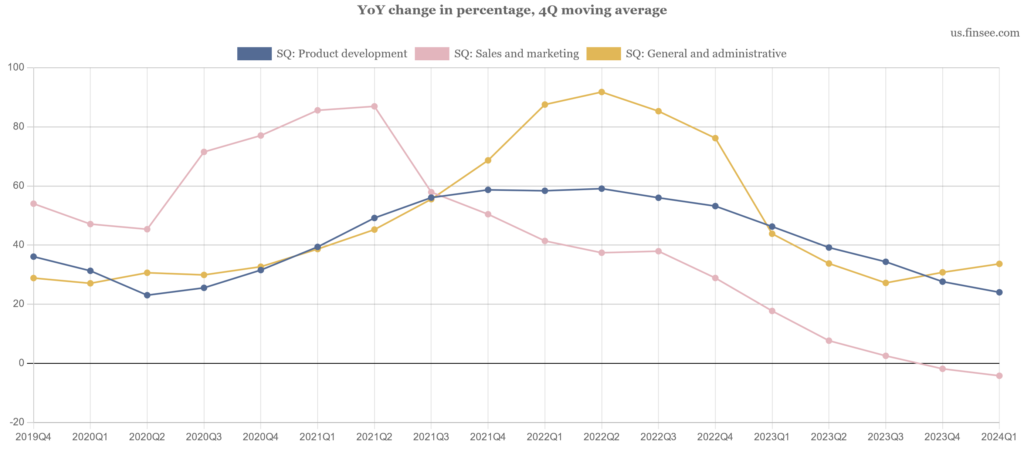

The marketing costs stopped growing in Q1 2023. Block commented on this in Q1 2024 quarterly report:

Cash App marketing expenses were down 18% year over year, driven primarily by a decrease in advertising costs as we have continued to focus on expense discipline, and a $27 million release of chargeback losses related to prior periods, which were partially offset by an increase in peer-to-peer processing costs. Other sales and marketing expenses were up 2% year over year. Other sales and marketing expenses primarily include expenses related to Square and TIDAL.

Product development and administrative expenses are still trending higher but at a lower pace. 4 quarters moving average:

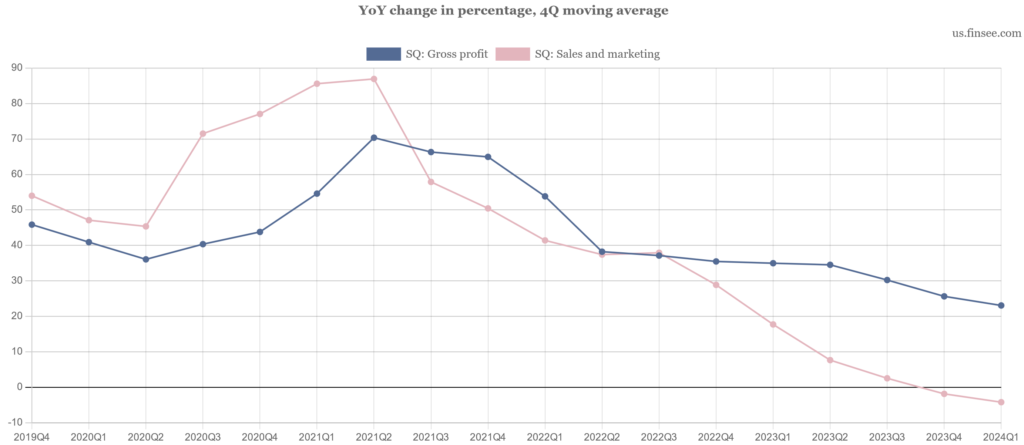

Growth rate suffered as a result of lower marketing costs. For gross profit it went down from 61.7% YoY in 2021 to 25.3% in 2023. The guidance for 2024 is just 17%.

4 quarters moving average growth:

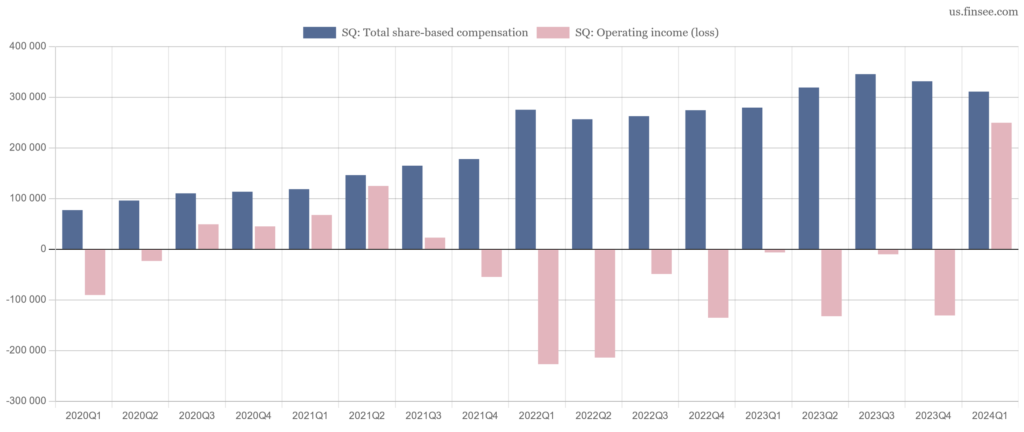

Share-based compensation puts heavy pressure on operating income but situation improved recently:

Segments

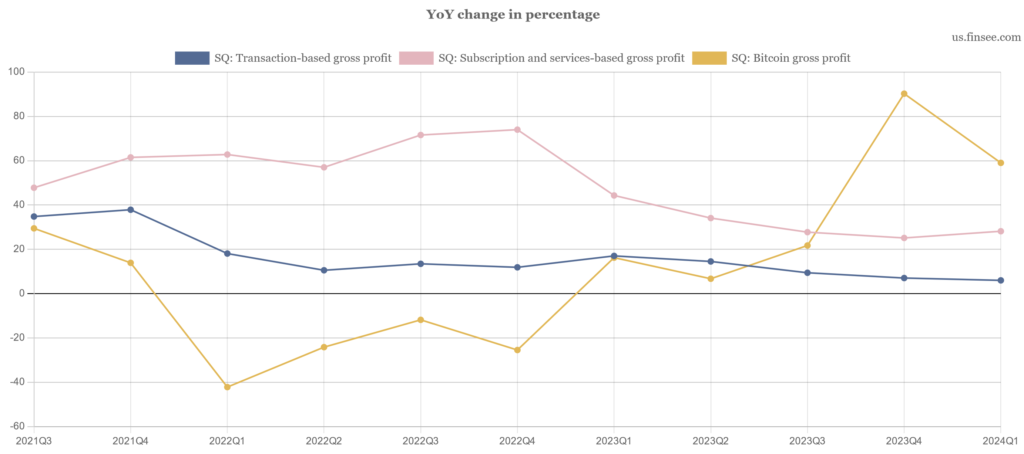

The Bitcoin segment is the fastest-growing. But it provides only 3.8% of gross profit. The most significant segment is Subscriptions which has above-average growth and brings the most money to Block.

Block operates 2 reportable segments:

1. Square – includes managed payment services, software solutions, hardware, and financial services offered to sellers, excluding those that involve Cash App.

2. Cash App – includes the financial tools available to individuals within the mobile Cash App, including peer-to-peer payments, bitcoin and stock investments.

The company has 4 operating segments:

1. Transaction-based – Block charges its sellers a transaction fee for managed payments solutions that is generally calculated as a percentage of the total transaction amount processed.

2. Subscription and services-based – revenue from Cash App Instant Deposit, Cash App Card, interest earned on customer funds, bitcoin withdrawal fees, Square Loans, the Company’s BNPL platform, TIDAL, and various other software as a service (“SaaS”) products.

3. Hardware – revenue from sales of magstripe readers, contactless and chip readers, Square Stand, Square Register, Square Terminal, and third-party peripherals.

4. Bitcoin – Block offers its Cash App customers the ability to purchase bitcoin, a cryptocurrency denominated asset, from the Company.

The hardware segment is almost immaterial with 0.5% of total revenue during Q1 2024.

Bitcoin and subscription operating segments show above-average growth, while the transaction-based segment is below average. The bitcoin segment adds a second layer of volatility because its growth rate follows the price of Bitcoin.

Most money comes from subscriptions and services. The bitcoin segment has a long way to go to become a significant contributor to the gross profit:

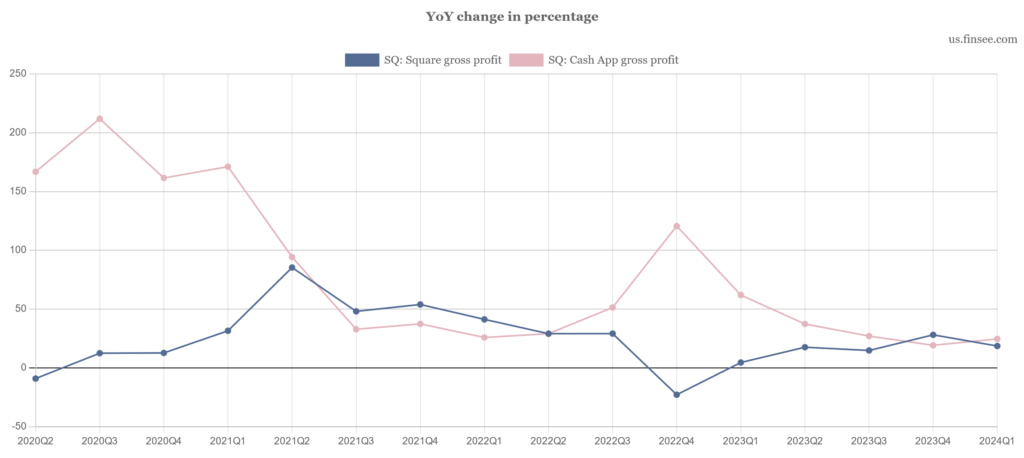

Cash App was growing much faster in 2020 and 2022 but now is mostly in line with the Square reportable segment:

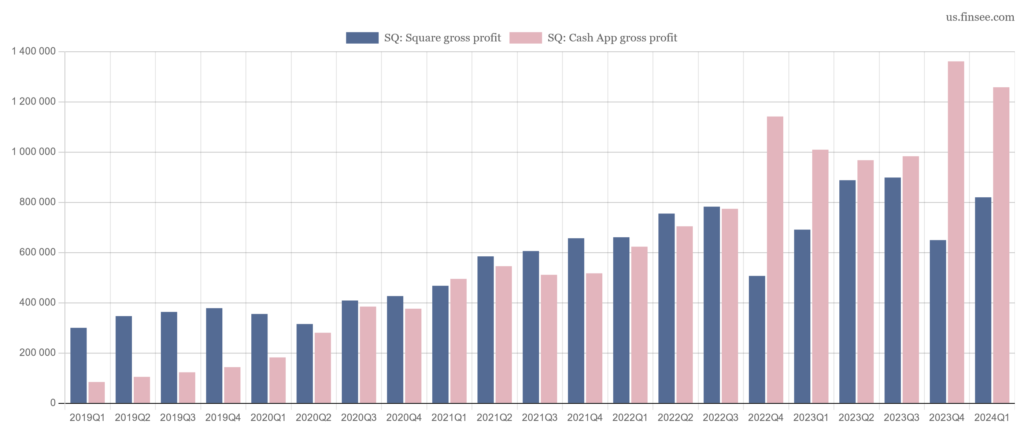

Starting from Q4 2022 Cash App became a bigger profit source than Square:

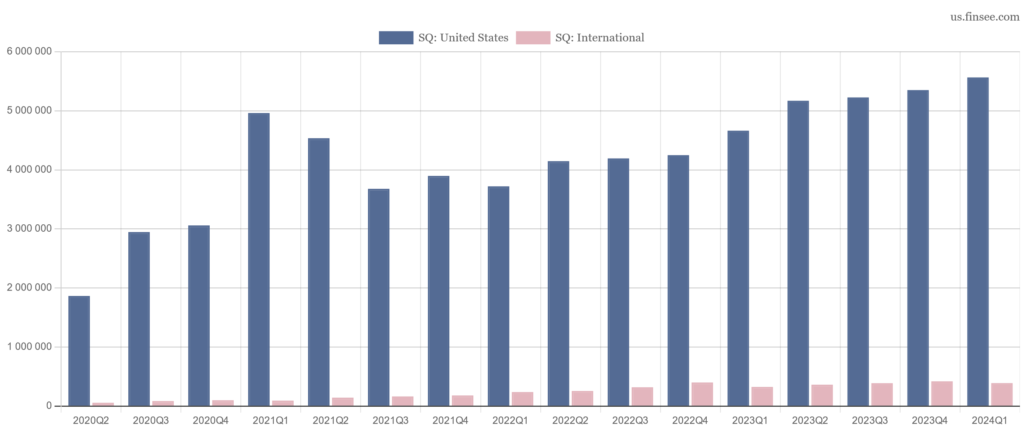

The US market is dominating Block’s sales. International revenue represented only 6.6% of the total during Q1 2024 and it grew at the same rate as USA recently.

Block disclosed that 13% of the Square segment gross profit came from international markets but we didn’t find a number for the Cash App segment.

Net revenue by geographic area:

Balance sheet

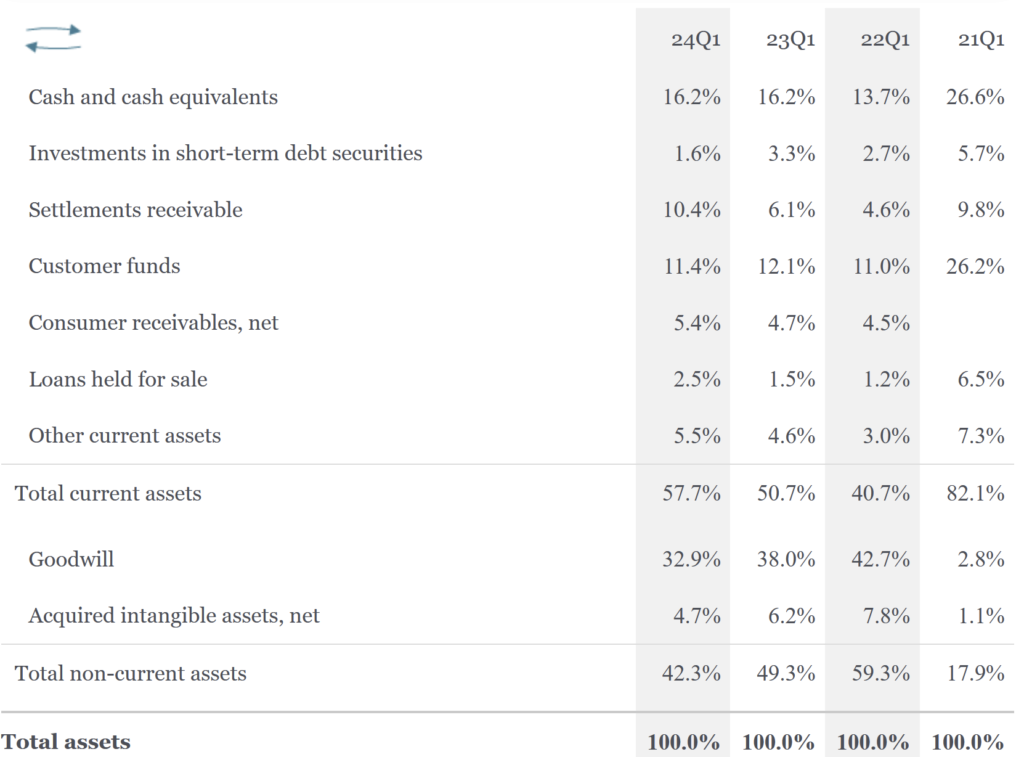

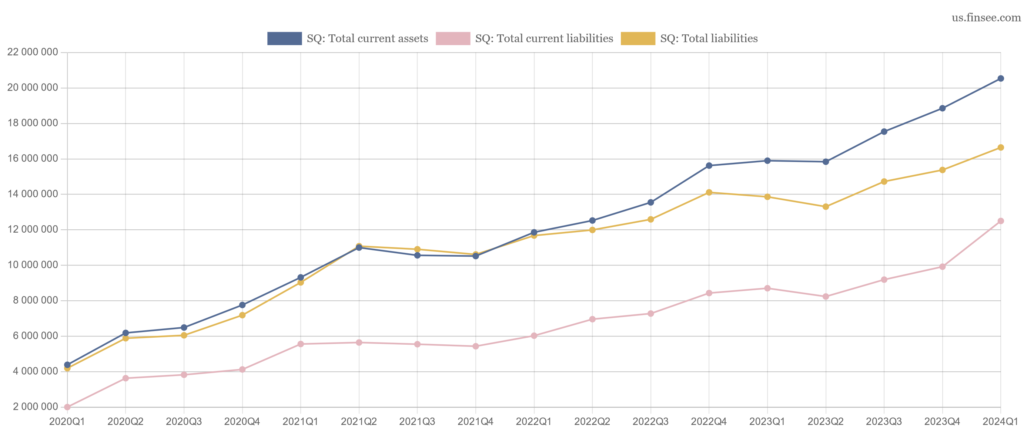

Block does not require big capital investments. Its liquidity seems adequate.

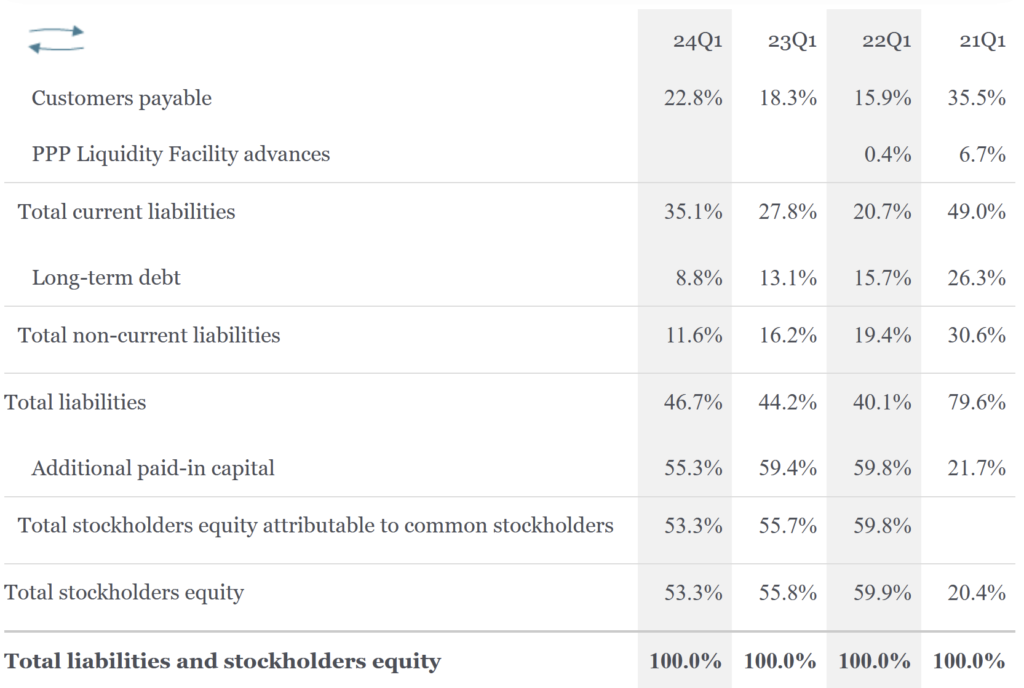

On the funding side, most money came from equity and short-term liabilities. The main change happened as a result of Afterpay acquisition in 2022, when shareholders of Afterpay received Block stocks. The table below shows only positions with a 5% or higher share of the total:

Current assets are higher than total liabilities. Long-term assets mostly consist of goodwill and intangibles:

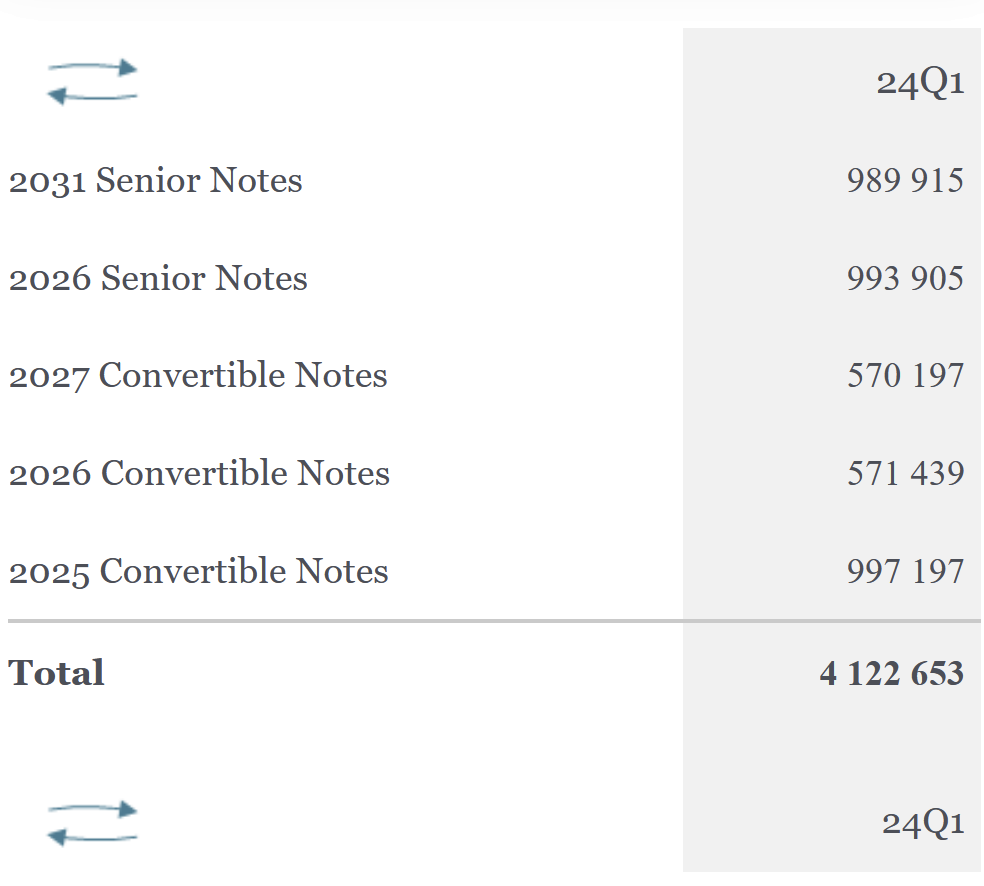

Debt repayments are spread for the next 7 years:

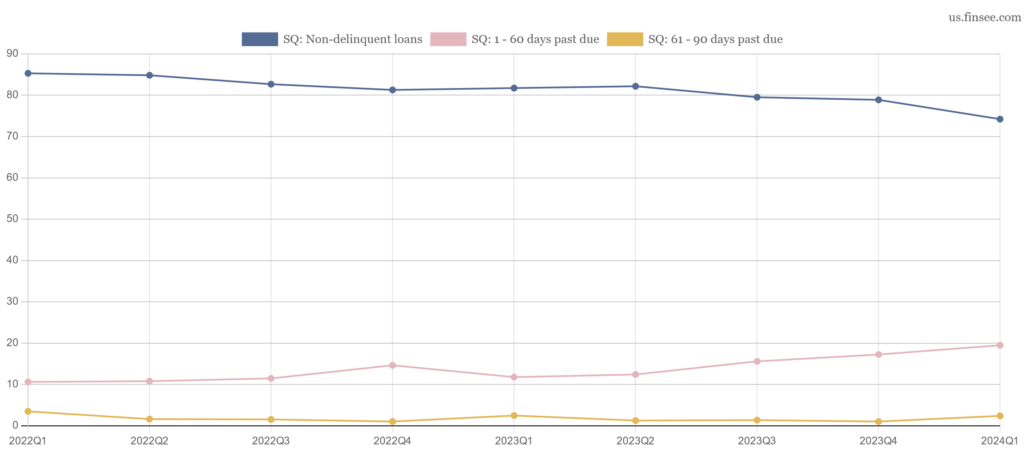

Consumer receivables ($2.1B on March 31, 2024) show a sign for worry: loans 1-60 days past due are rising much faster than non-delinquent loans and represent 19.5% of the total.

61-90 days past due are 2.4% and more than 90 days are 3.9% of the total with the latter category possibly accumulating loans from previous periods.

Share of total consumer receivables in percentages:

Cash flow

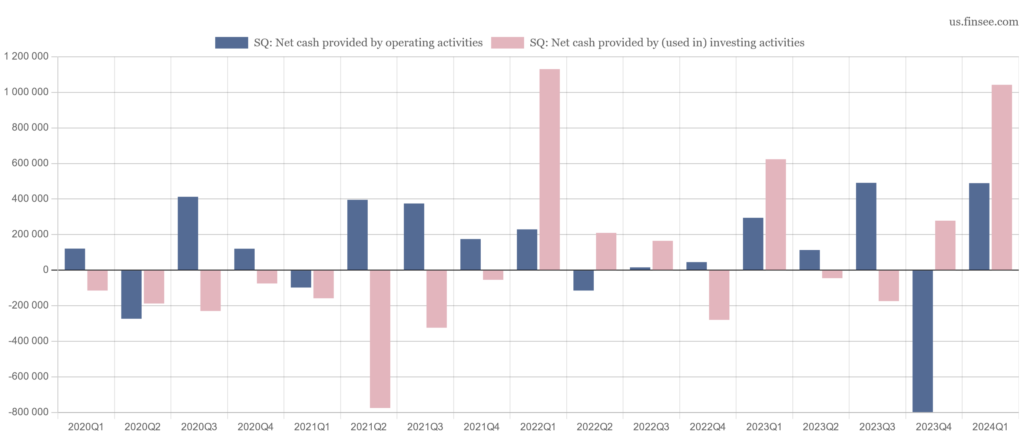

Since 2022 the company began to receive significant amounts of cash from both operating and investing activities.

Negative operating cash flow in Q4 2023 was the result of other cash adjustments, higher loan originations, and other assets and liabilities.

Investing cash flow mostly comes from principal repayments and sales of consumer receivables.

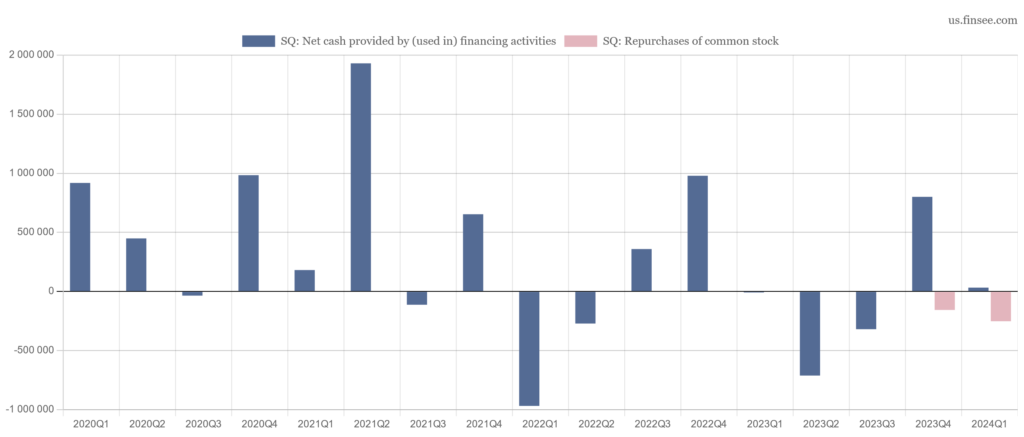

As a result, Block doesn’t need much external financing and even began to repurchase its common stock recently:

Summary

Block shows many signs of a mature company: strict cost controls, lower revenue growth and positive investing cash flows as a result of a capital-light business model. And at the same time, there is a double Bitcoin volatility: from coins on the company’s balance sheet and from customers’ transactions, which move with the price of Bitcoin.

Possible regulatory scrutiny and tighter KYC controls add to the risks of the business.

Whatever Dr. Burry discovered remains elusive for us. We do not see neither significant growth nor a strong value proposition to recommend Block shares as an investment right now.