Review date: June 12, 2024

All numbers on charts are in thousands USD, except when stated otherwise.

Verdict:

DoubleVerify has the potential for a huge success but likely only after this year.

Pros:

- leader in its niche with strong AI potential;

- excellent balance sheet and cash flow.

Cons:

- sales growth has fallen rapidly while expenses are accelerating;

- main growth drivers (social and AI) are still small and unable to lift the whole business this year.

How DoubleVerify could benefit from AI?

DV helps advertisers verify that their ads were viewed by real people and avoid running those ads next to objectionable content.

This is important because otherwise ad platforms like Google or Meta state the number of ad views and bill advertisers without meaningful control.

The main advantage of DoubleVerify is it knows what happens with customers’ ads on each platform in real-time: social, video, web, and even in retail locations. DV has data integrations with Google, Meta, TikTok, Netflix, Walmart, and many others.

AI and Machine Learning have already proved to bring huge benefits to digital ads.

Google Ads added smart bidding to their campaigns in 2016 and it has been a huge success for both the company and advertisers. The main reason is humans are unable to act as quickly and efficiently in ad editing and settings change. But Google is constrained by its own platforms while DoubleVerify works with every big platform.

Imagine you are a small accounting company and an Instagram blogger with 5k subscribers posted about how hard it is to find a good accountant in your area. AI or machine learning solutions could:

1. Place your ads before you are even aware that something is going on.

2. Decrease the budget for other social networks and increase for Instagram.

3. Check if this discussion later goes to other platforms and move the budget there.

DoubleVerify acquired Scibids in August 2023. This company specialised in AI for advertisers and showed very promising results. For example, in 2023 Icelandair tested Scibids AI in 11 target markets. The result was a 70% decrease in cost per flight booking, representing a tenfold improvement in ROI from digital advertising.

During the Q1 2024 earnings call DoubleVerify’s CEO said that Scibids was sold to 19 advertisers, including 9 from the top 100. The average return on investment was $4 for every $1 invested in Scibids. An extra advantage of Scibids – it does not rely on third-party cookies, which will be phased out soon in most browsers.

CEO comments about the importance of Scibids acquisition are on pages 2-3 of the Q2 2023 earnings transcript (pdf file).

Scibids also works in retail media networks (ads in Target, Walmart, Amazon, and others), where DoubleVerify has a strong presence. It could help advertisers like Colgate, Mondelez, or Unilever better connect ads in these shops with purchase data.

Scibids is expected to bring $15-17M of revenue in 2024 or just 2.4% of the total, representing a huge longer-term growth opportunity if implemented according to expectations.

Main risks

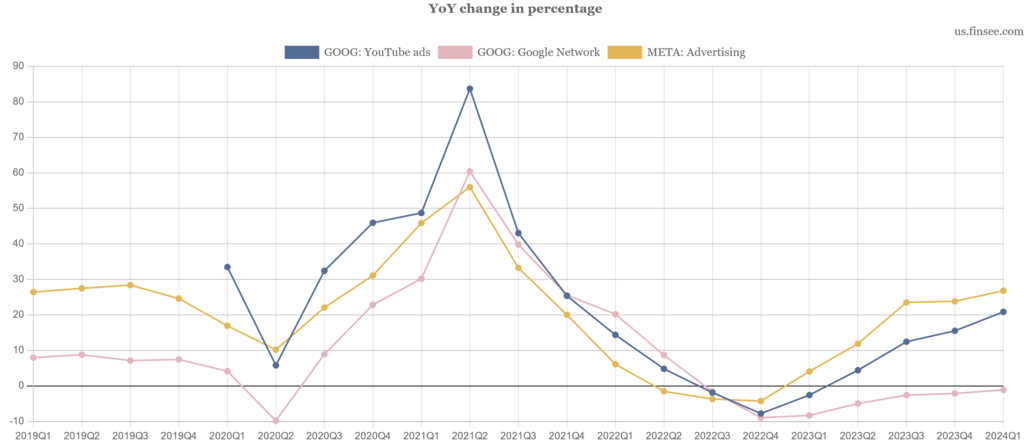

Unfavorable shift in ad spending

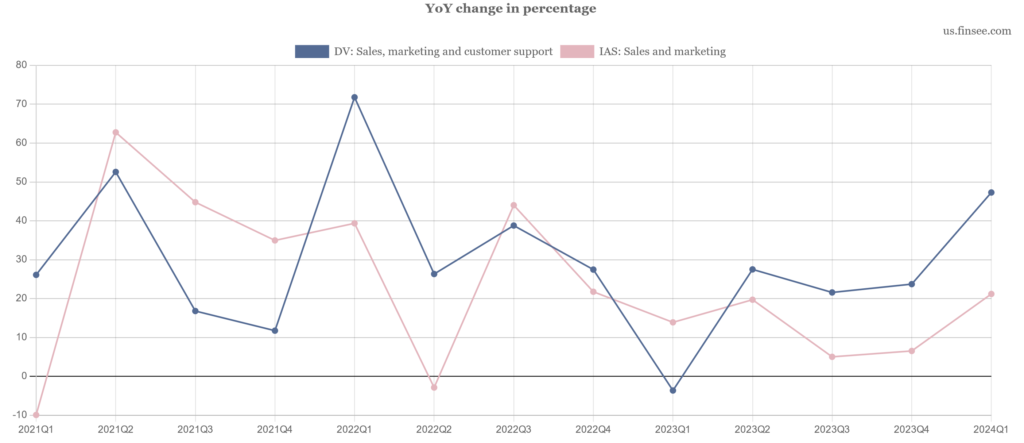

Ads on websites are the main revenue source for DV, while advertising budgets went from websites to social in 2023-24. YoY growth rate of Google Network (ads on third-party websites) vs YouTube and Meta:

Other social platforms (Snap, Pinterest) show a dynamic similar to YouTube and Meta.

As a result, social revenue increased 51% YoY for DoubleVerify in Q1 2024 and 48% in 2023. But it is still a small segment, unable to lift overall sales much.

Now ad money is going into a new hot area: video ads on streaming platforms like Netflix and Amazon Prime. DoubleVerify measures streaming too, the problem is that these platforms are much safer than social or websites. Advertisers know in which movies their ads are shown and the chance of bot views is low. This leaves measurement as a main revenue source for DV in streaming video.

During the Q1 2024 earnings call CFO said that DoubleVerify earns a lower fee in social media measurement.

In our view it creates a challenge for the company:

1. Future growth is expected from lower-fee segments.

2. While AI is still a small part of business.

Possible solutions:

1. As CEO answered a question about platform mix: when too many advertisers go into one platform, this platform becomes overpriced and the dynamic starts to shift back. So this issue could be temporary with websites providing more ROI for advertisers in the future.

2. Scibids AI has the potential to increase revenue and margins materially after a few years.

Potential conflict of interest

Scibids acquisition could create a situation when DV will verify its own work:

For example, Scibids AI is tasked with increasing the number of ad views and DoubleVerify confirms that your ads reached more real users.

This is only a potential situation and many advertisers will use Scibids to optimise conversions, which are confirmed by advertisers themselves, not by DV. Also, DV’s data is important for Scibids to bring better results, so we think it’s highly unlikely that an advertiser will use Scibids but will stop purchasing other DV products. Yet this is a risk to consider.

Segments

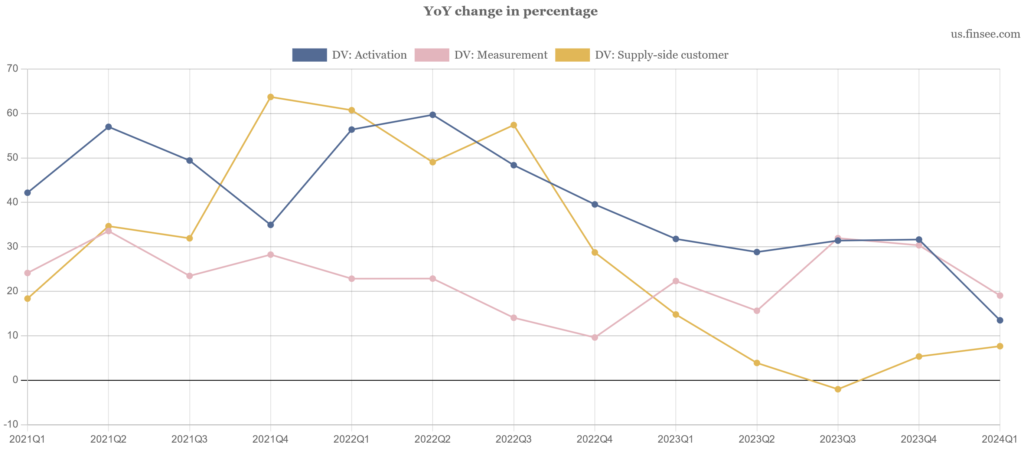

Activation is the main cash cow and it’s growth is slowing rapidly

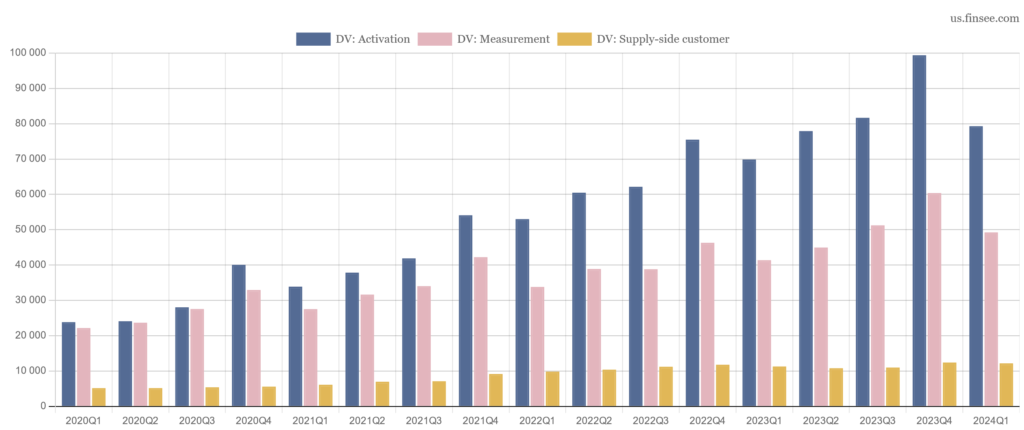

DoubleVerify reports revenue by customer type:

1. Activation – evaluating the quality and performance of advertising inventory that advertisers consider purchasing. It mainly answers the question: is this website or channel suitable to show your ads?

2. Measurement – measuring the quality and performance of ads purchased directly from digital properties, including publishers and social media platforms. It mainly answers the question: how many times did humans view your ads?

3. Supply-side customer – arrangements with publishers and other supply-side customers to provide them with software solutions and data analytics. These are agreements with social networks and other platforms, which want to bring in more advertisers.

Activation products are premium priced ($0.21 vs $0.08 per 1000 views in Measurement) and they bring the most revenue:

Which creates a problem, because Activation growth is falling fast due to the factors we pointed in Risks:

Growth drivers, according to the Q1 2024 earnings call:

Social (49% of Measurement revenue) +51% YoY. 80% of Social revenue came from Meta and YouTube with TikTok a distant third.

Authentic Brand Suitability (centralised brand safety platform, 55% of total Activation revenue) +12% YoY.

Retail media networks (ads in Target, Kroger, Macy’s, Dollar General, Walmart, Amazon, and others) +45% YoY in Q1 2024, down from +100% a year ago. A year ago sales in this category were expected to be $30-40M per year.

Connected TV (CTV) +45% YoY.

The main slowdown came from a handful of biggest retail and CPG (consumer packaged goods) advertisers.

DoubleVerify doesn’t report sales by region. The only metric provided during the earnings call is that international Measurement revenue share was 31% in Q1 2024 up from 26% in Q1 2023. The growth rate is 40% YoY.

Profit and Loss

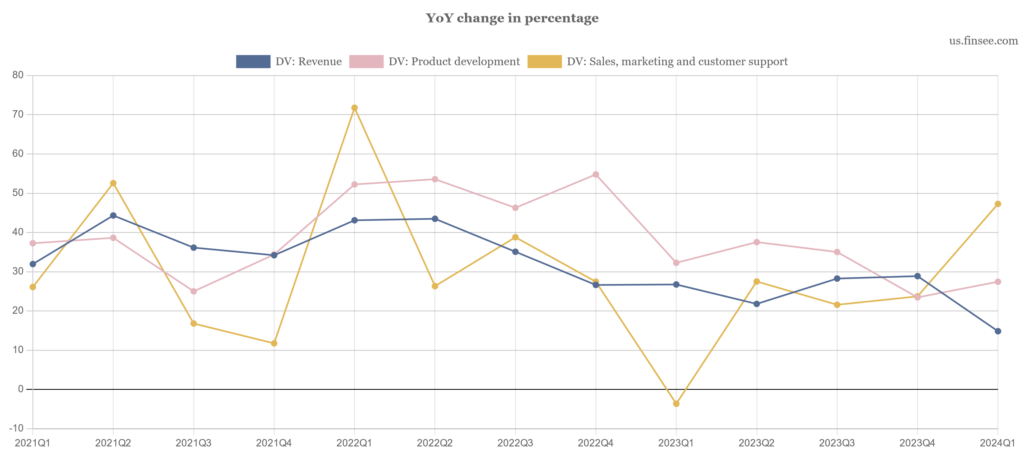

stock-based compensation, marketing, and R&D expenses are rising much faster than sales

DoubleVerify’s sales growth slowed to 15% YoY during Q1 2024 from 27% a year earlier. The company guided Q2 growth at 15% and 2024 full year at 17%, meaning this trend could bottom mid-year.

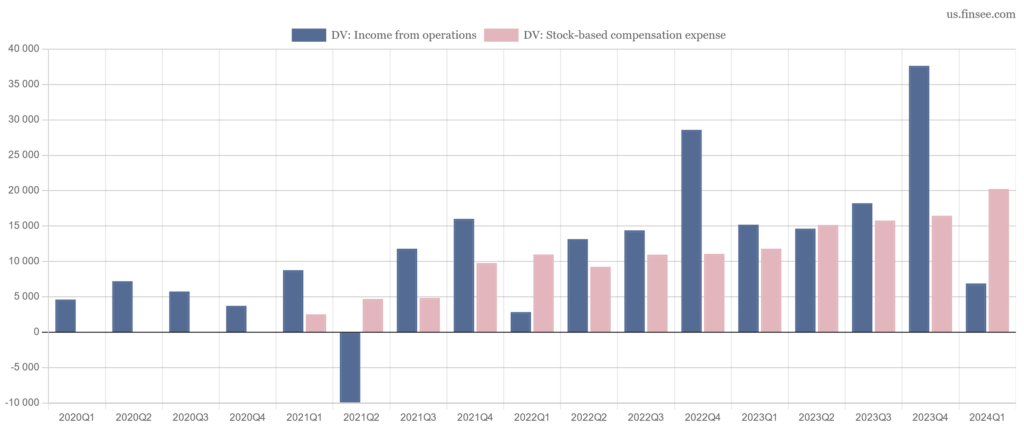

Marketing and product development expenses are accelerating. If the company doesn’t lift sales soon, its net income could face significant pressure:

DV gave the following explanation in the Q1 2024 earnings call:

Research and development expenses increased due to investments in AI and machine learning engineering resources. Sales and marketing expenses increased as we invested in additional resources to promote and sell our most recent product launches, including Scibids around the globe.

What’s worrying is that DoubleVerify’s main competitor Integral Ad Science (IAS) is also increasing marketing spending, which could mean that the market will face higher competitive pressure rather than new products. This is a risk to watch for the next quarters.

Another pressure on net income is added by stock-based compensation, which increased 71% YoY during the last quarter, becoming three times bigger than operating income:

Next quarter’s mid-point guidance is 61% YoY growth of stock-based compensation with 15% growth in sales, so this problem is not going away soon.

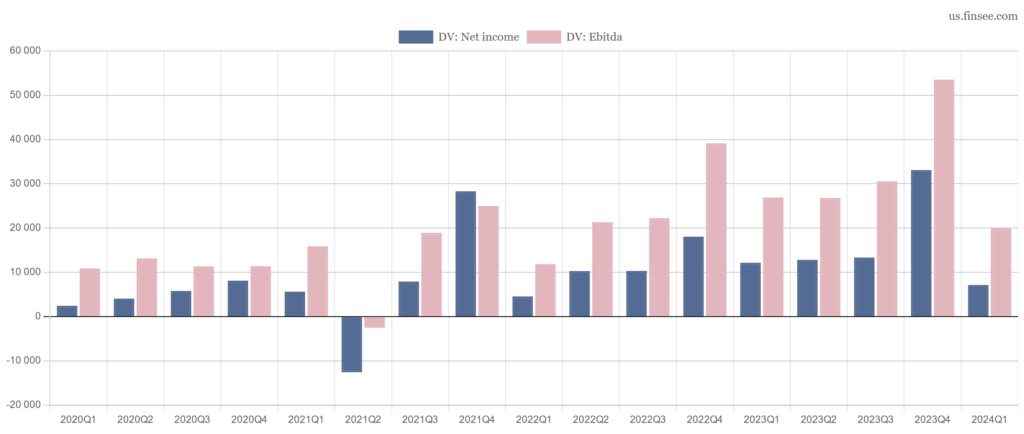

As a result, during Q1 2024 net income was 41% lower and Ebitda 25% lower YoY:

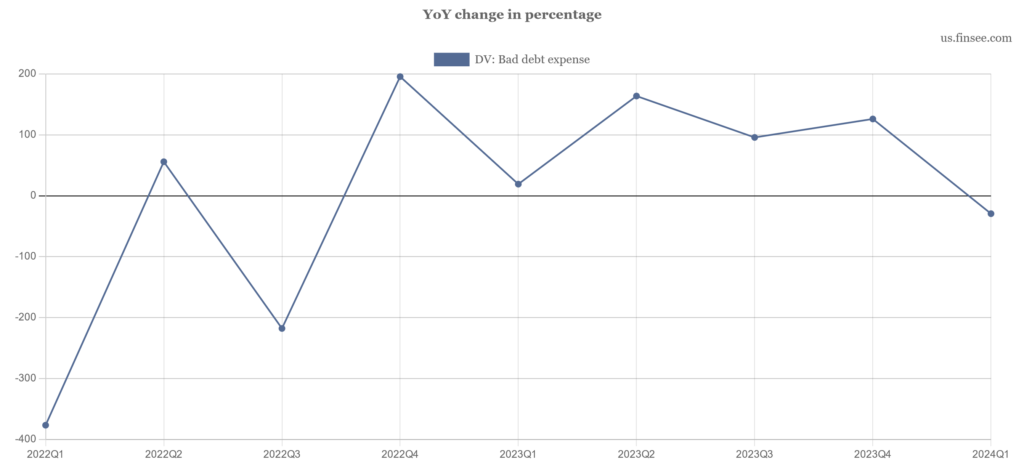

Bad debt expense was $907k in Q1 2024 or just 0.6% of sales and it went down YoY after rising significantly during the previous year:

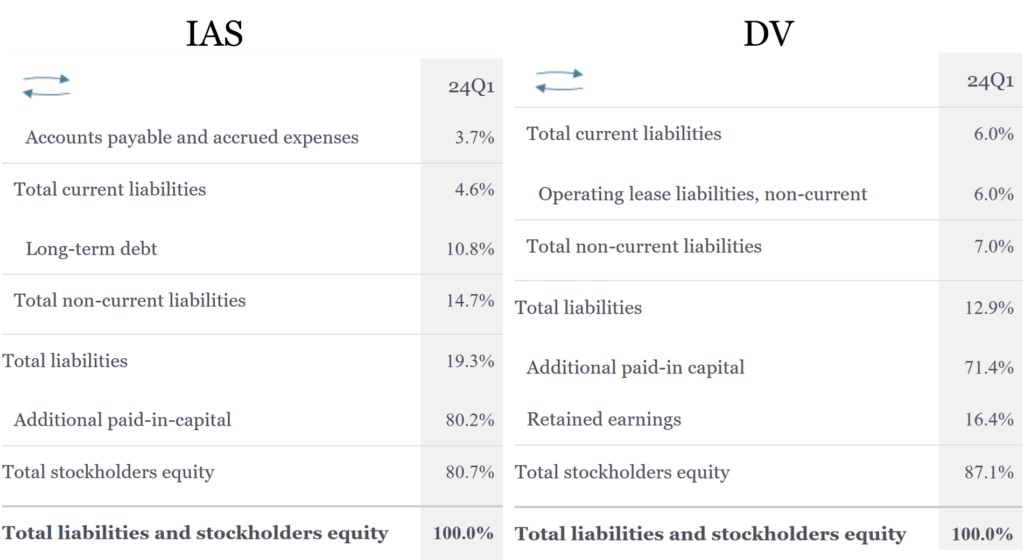

Balance Sheet

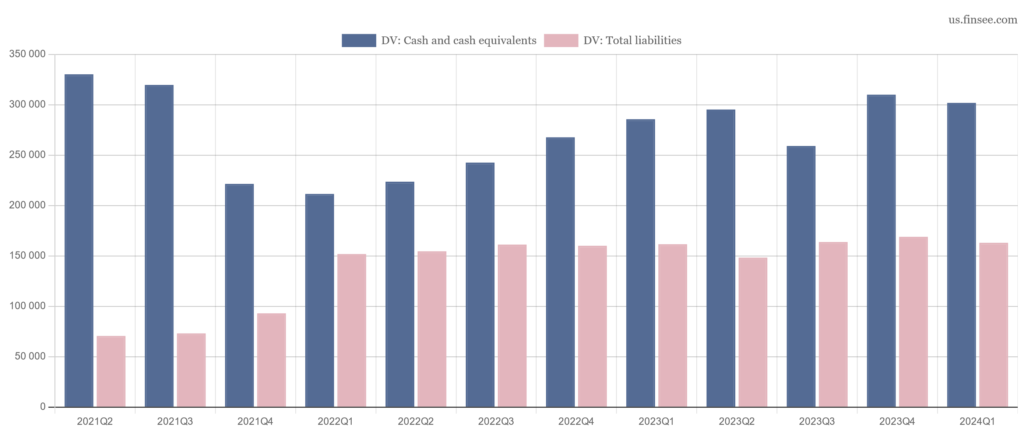

DoubleVerify has an exceptionally solid balance sheet

Cash is almost two times higher than total liabilities, making any balance sheet risks very low:

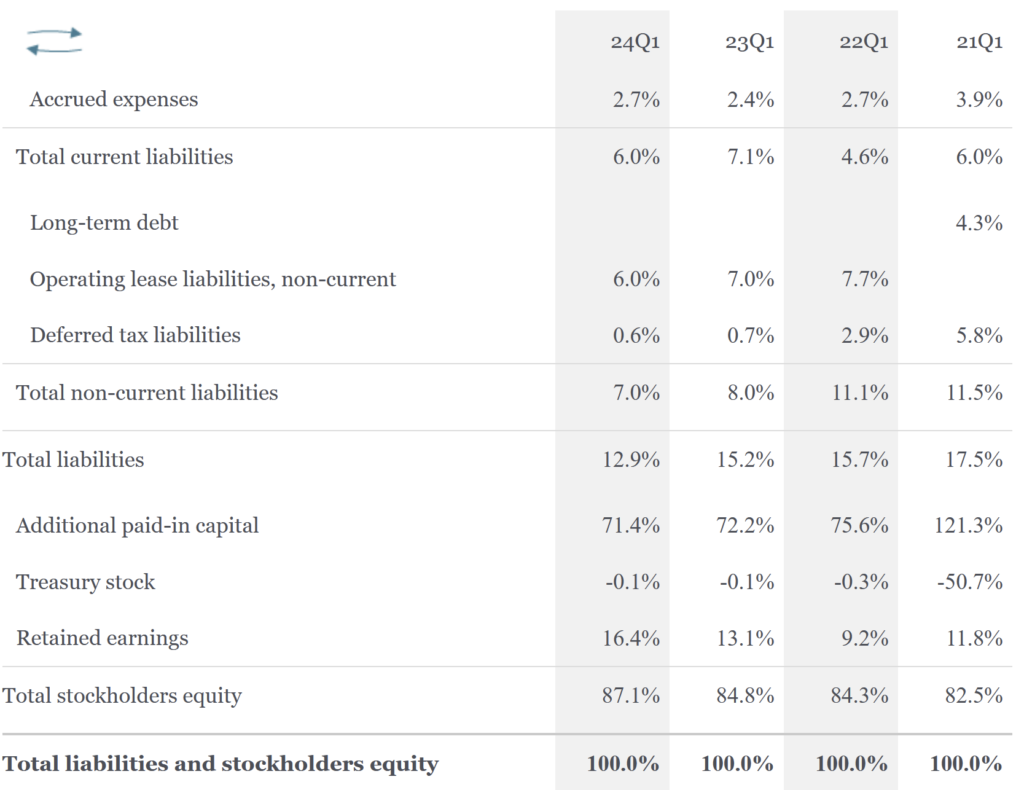

The main funding comes from issued stock, 71.4% of total liabilities and equity, retained earnings are a distant second at 16.4% and liabilities make up just 12.9% of total. Almost half of liabilities consist of operating leases.

Share of liabilities and equity, only articles with 3%+ share are included:

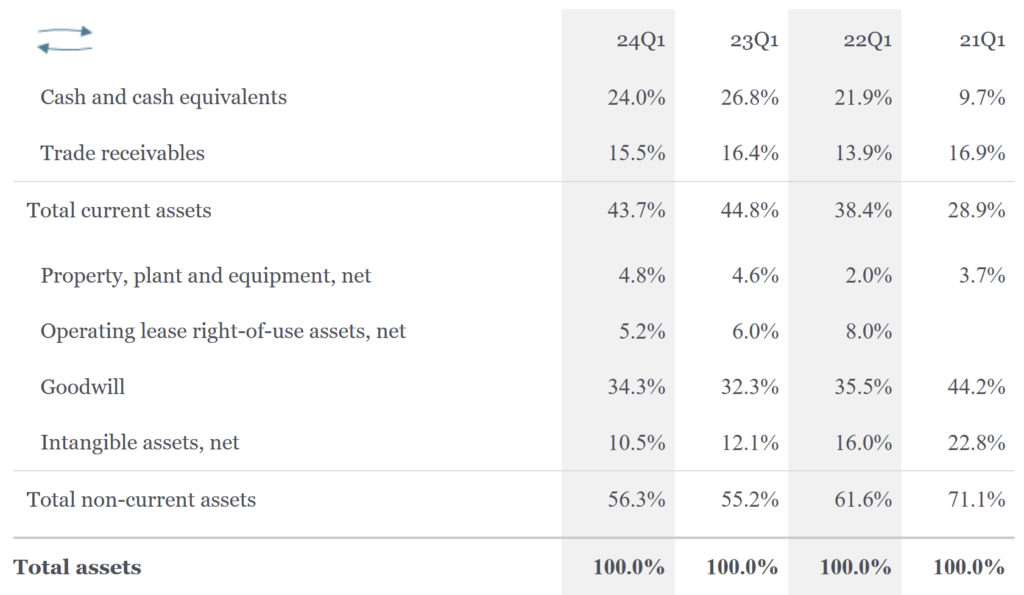

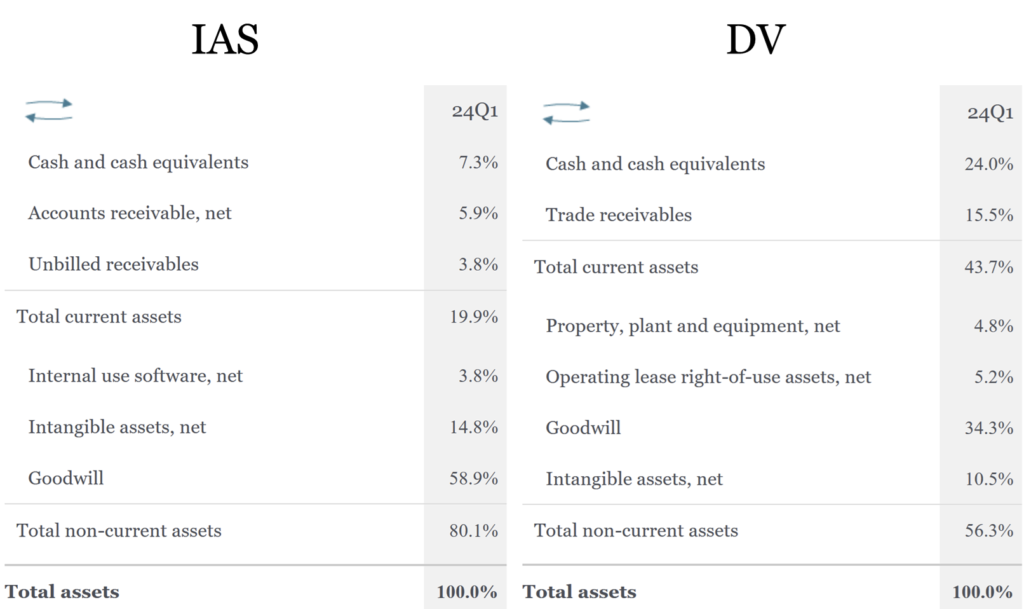

44.8% of assets are invested in goodwill and intangibles, 24% in cash and 15.5% are trade receivables. Bad debt expense is low, so there is a good chance they will be collected.

Share of assets, only articles with 3%+ share are included:

Cash Flow

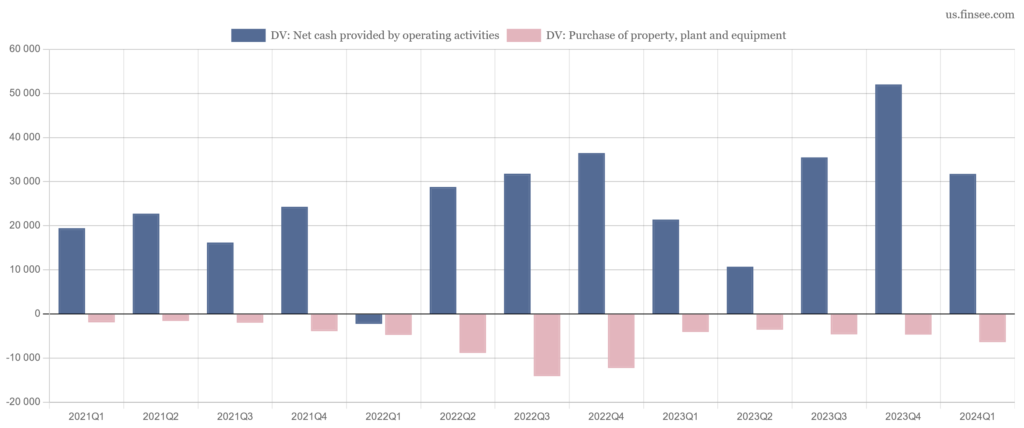

DoubleVerify generates enough cash to cover its needs but doesn’t return money to shareholders yet

Cash flow from operations brings in $30-50M per quarter. DV invests $3-6M per quarter in property and equipment, with the most money going into capitalised software.

DoubleVerify made two significant acquisitions in 2021 and 2023 using $217M in cash and issuing additional shares.

As a result, the company uses only small amounts of external financing after receiving $269M from IPO in 2021.

DoubleVerify doesn’t pay dividends and makes tiny share repurchases.

Competition

The main competitor is Integral Ad Science (IAS).

| DV | IAS | |

| Market Cap | $3.17B | $1.44B |

| Enterprise Value | $2.87B | $1.47B |

| Forward P/E | 55.5 | 38.8 |

| Trailing Price to Free Cash Flow | 31.7 | 11.1 |

DV is the market leader, has zero debt, higher sales growth, and profitability. IAS free cash flow is equal to DV, despite two times cheaper valuation.

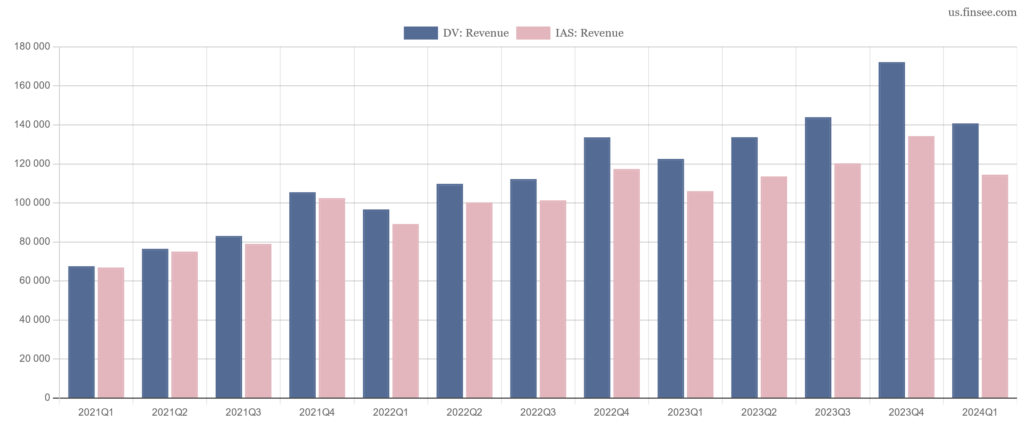

The two companies have almost similar sales but DV has been increasing the gap since 2022:

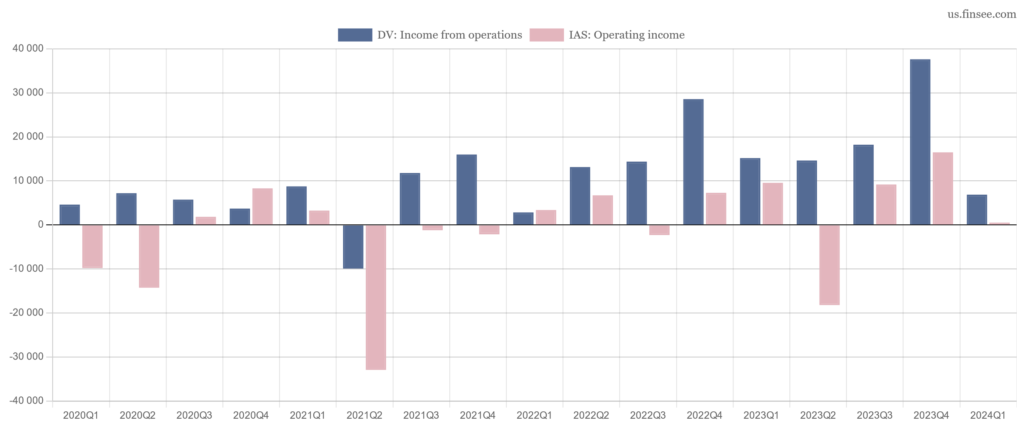

DV’s advantage in profitability is much bigger. We compare operating income because IAS net income is even more negatively affected by interest on debt:

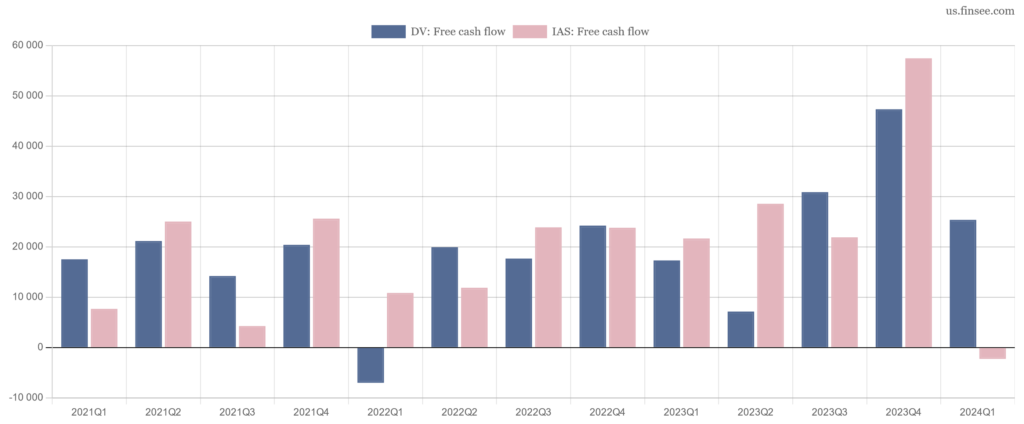

IAS amortises its intagibles faster and has higher working capital. As a result, both companies have similar free cash flow:

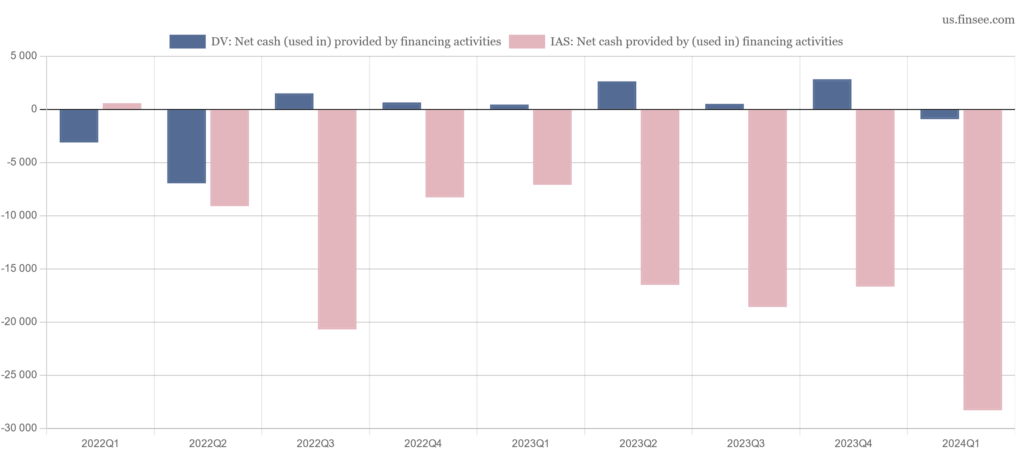

IAS has to repay its debt, which takes significant amounts of cash each quarter. DV’s debt is zero.

This long-term debt is due in 2026 and it creates the main difference between the two companies’ liability structures:

DV has even bigger advantage on the assets side: IAS cash is lower than debt and it has higher share of goodwill and intangibles:

We think DoubleVerify is a clear winner in this comparison. Integral Ad Science could be considered a cheaper alternative at a price of 11 trailing free cash flows.

Summary

There is a high chance things will get worse for DV in the near term before becoming much better in the mid-term.

Their main growth drivers: social, video, Scibids AI, and retail media are still small contributors to overall results. As they gain a higher share things will turn to the upside again. We have especially high hopes for an AI solution, which could go the same way as Google’s smart bidding since 2016: bringing more money to advertisers, platforms, and DoubleVerify by showing more relevant ads.

Meanwhile, we continue to monitor DV’s progress either for the first signs of a turnaround or for a lower price, if it comes earlier.