Review date: May 22, 2024

All numbers on charts are in thousands USD, except when stated otherwise.

Verdict:

First Solar plans to have strong growth in 2024. Beyond that things become uncertain: they have a huge backlog but new bookings were much lower during late 2023 – early 2024. And there were no new bookings in April 2024, the first time in several years.

Pros:

- strong revenue growth and profitability;

- $1.4B net cash position;

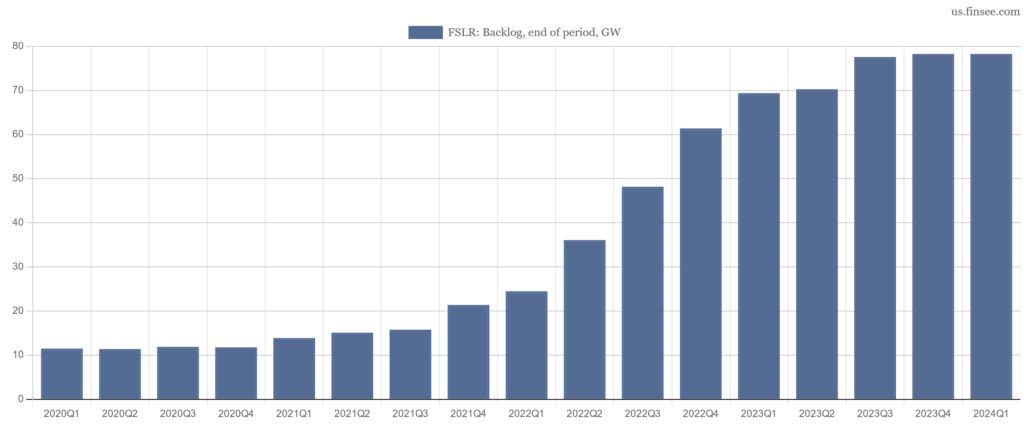

- $23B backlog;

- capacity is expanding.

Cons:

- new net-bookings slowed dramatically from Q4 2023;

- accounts receivable grow much faster than sales, which is weird during the period of strong sales growth.

Segments

First Solar is highly concentrated on one niche: almost all sales come from the solar modules segment in the United States

The company operates in two reportable segments:

- Modules – design, manufacture, and sale of CdTe solar modules, which convert sunlight into electricity.

- Other – certain project development activities, operations and maintenance (“O&M”) services, the results of operations from PV solar power systems the company owned and operated in certain international regions, and the sale of such systems to third-party customers.

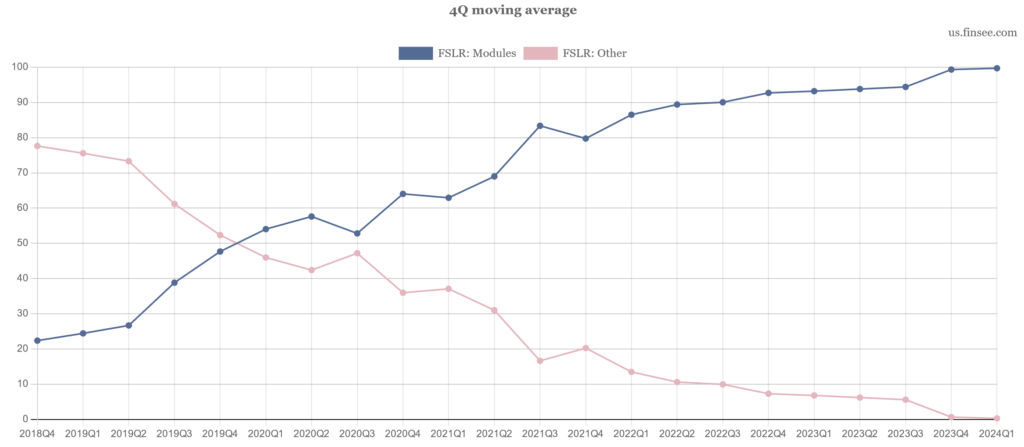

Until 2019 the Modules segment was smaller, but First Solar decided to concentrate on this segment and now it represents 99.9% of sales. Share of First Solar sales by segment in percentages:

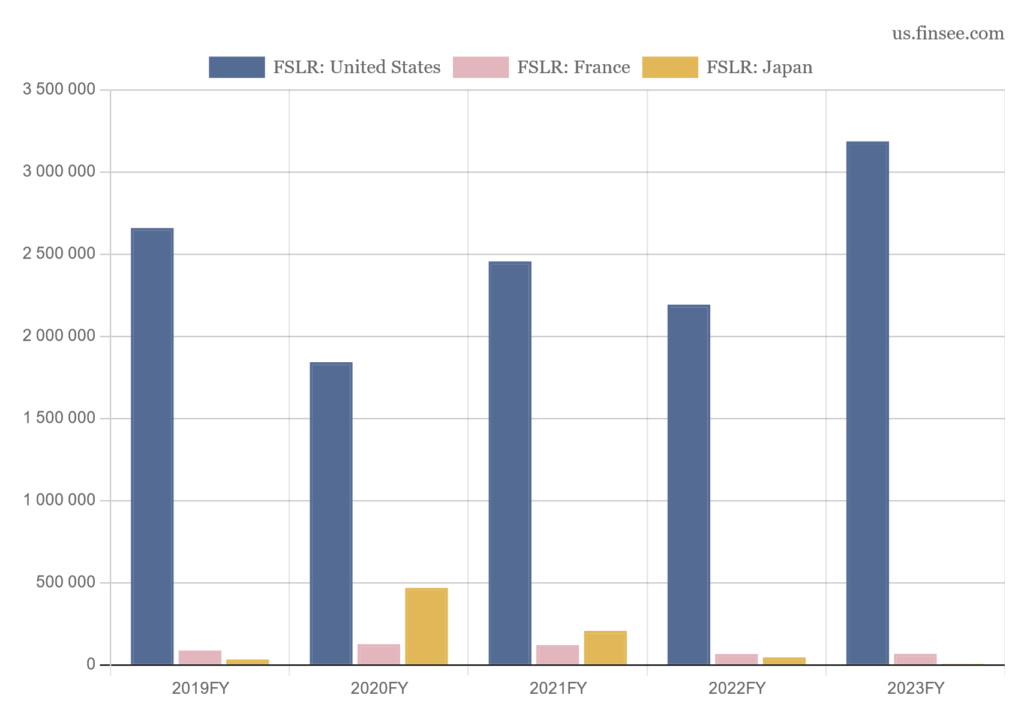

The United States is dominating in sales by country with 96.1% of the total in 2023. From time to time FSLR has big projects in other countries:

Profit and Loss

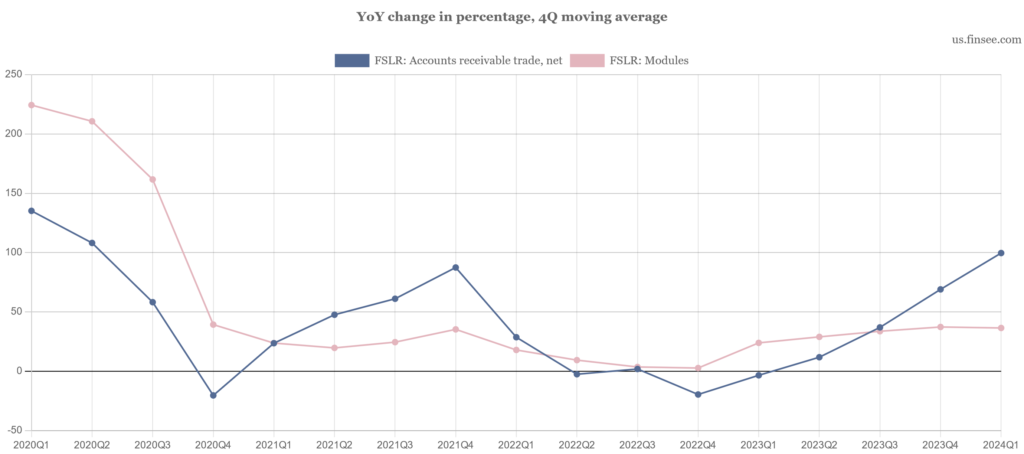

Sales are growing fast and profitability has improved much, but there are two questions: how long will a fall in new bookings last, and when will extra receivables turn into cash?

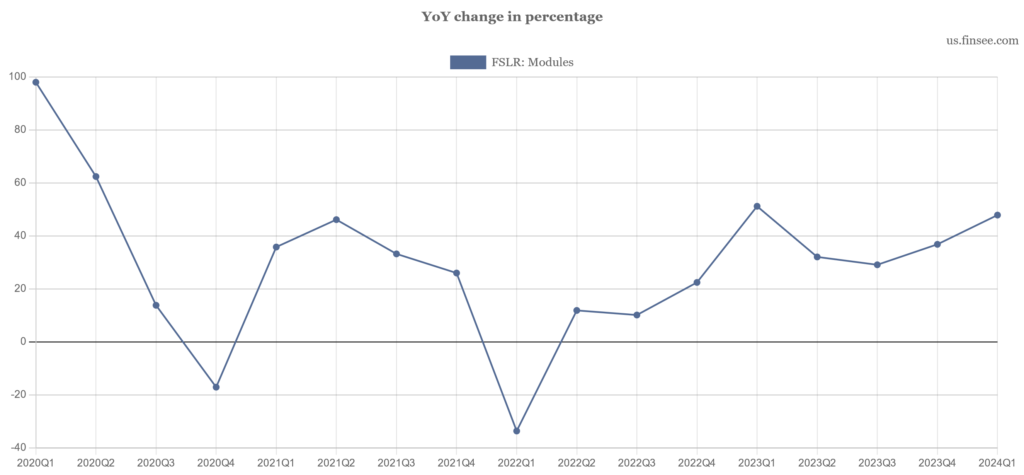

Looking at sales, we will concentrate on the Modules segment, because other sales are almost immaterial now. The sales growth is very strong recently:

But there are two big issues: new net-bookings and accounts receivable.

New net-bookings dropped 3.7 times YoY during Q1 2024 to 2.7 GW. In April 2024 there were no new net-bookings at all: the first such occasion in at least 5 years.

The backlog reached 78.3 GW ($23.4B) at the end of March 2024 with contracts stretching through 2030:

So even without new net-bookings First Solar has many orders to fulfill. But it seems that it takes more and more effort to keep sales growing at the current rate: accounts receivable are rising much faster than Modules sales, doubling YoY during the last quarter. FSLR gives longer payment options to customers.

4 quarter moving average growth:

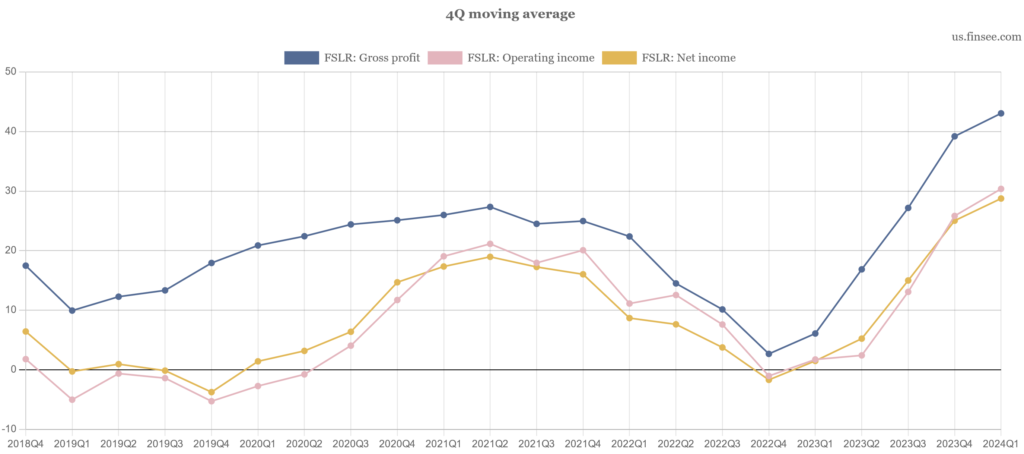

Profitability has significantly improved recently.

Share of net sales in percentages, 4 quarter moving average:

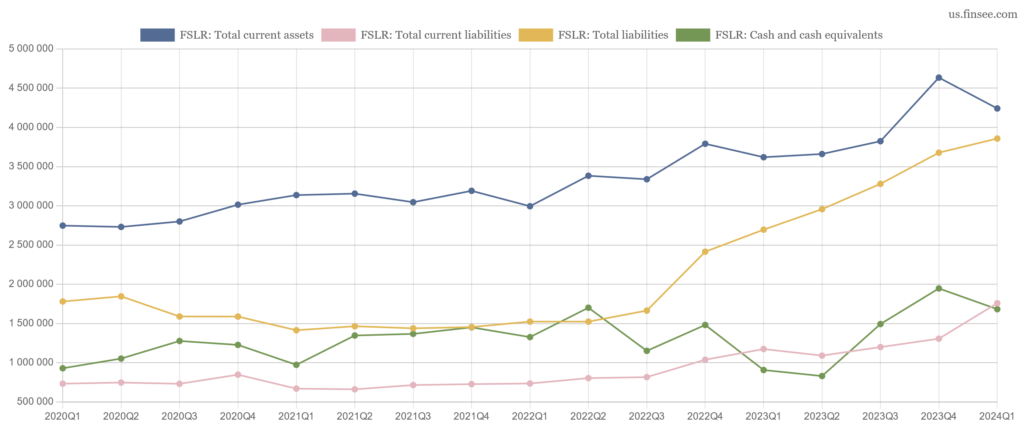

Balance sheet

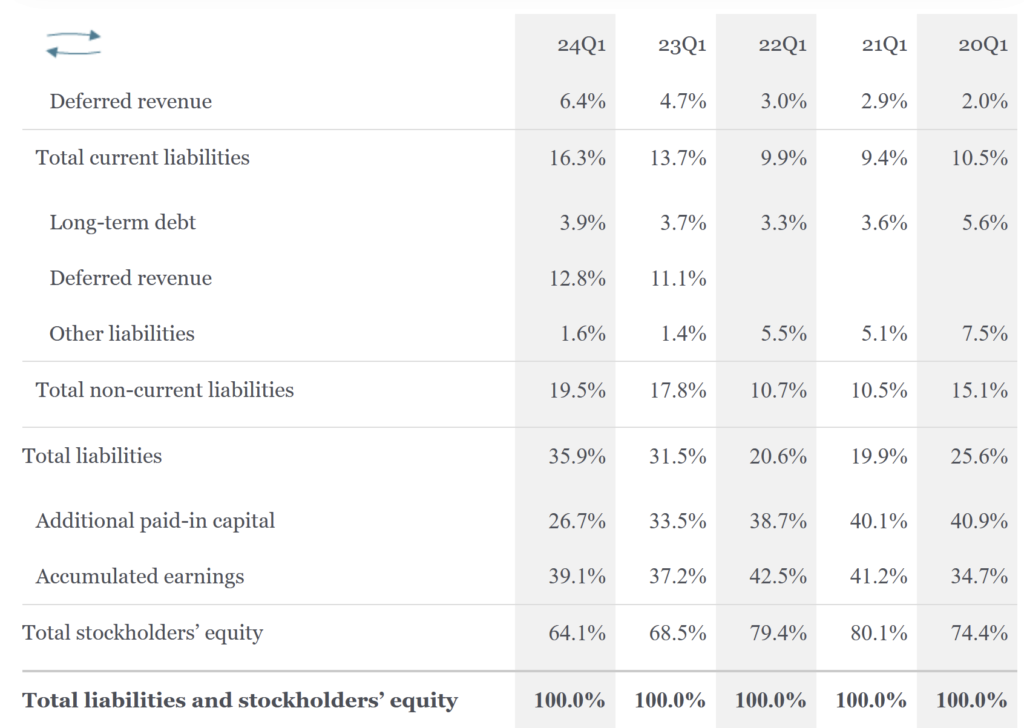

Balance sheet is very healthy with net cash position

First Solar is funded mostly by accumulated earnings. The debt level is very low.

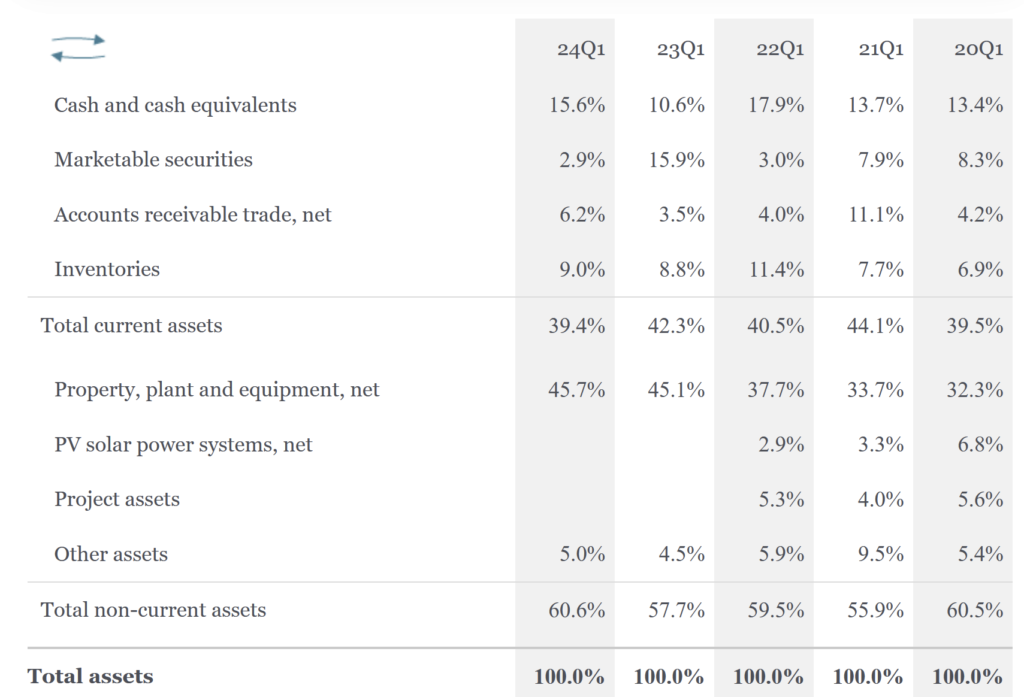

The table below shows only positions with a 5% or higher share of the total:

Property and equipment is almost half of all assets. Cash is four times higher than debt and overall current assets cover all liabilities.

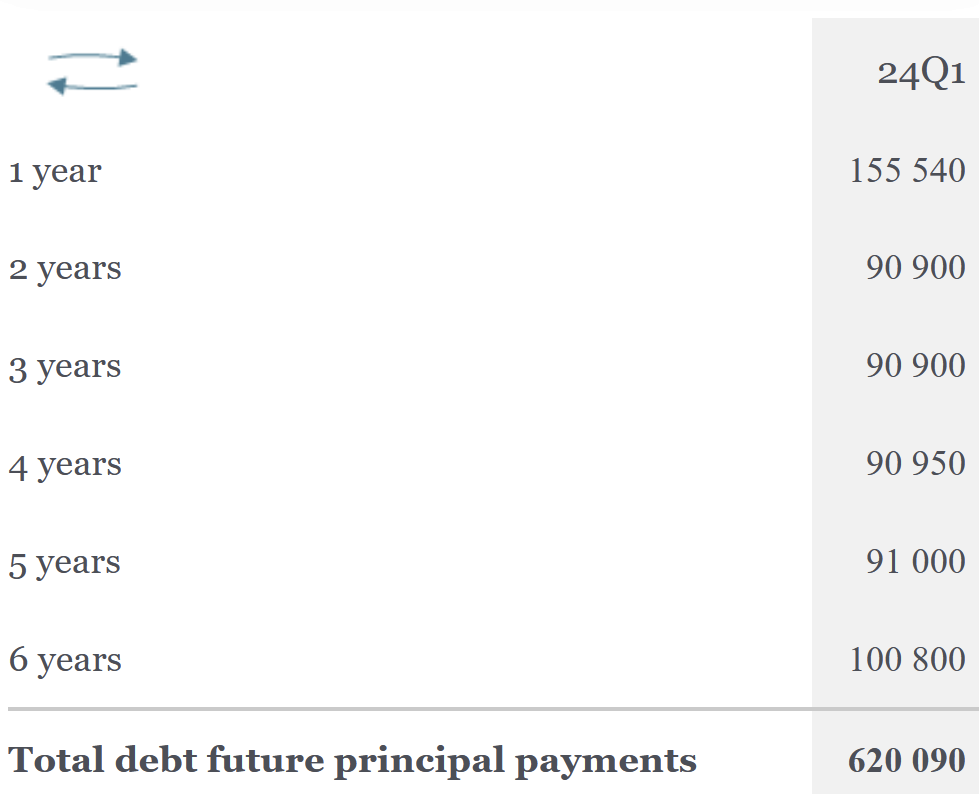

Debt repayments are small and spread almost evenly for the next 6 years:

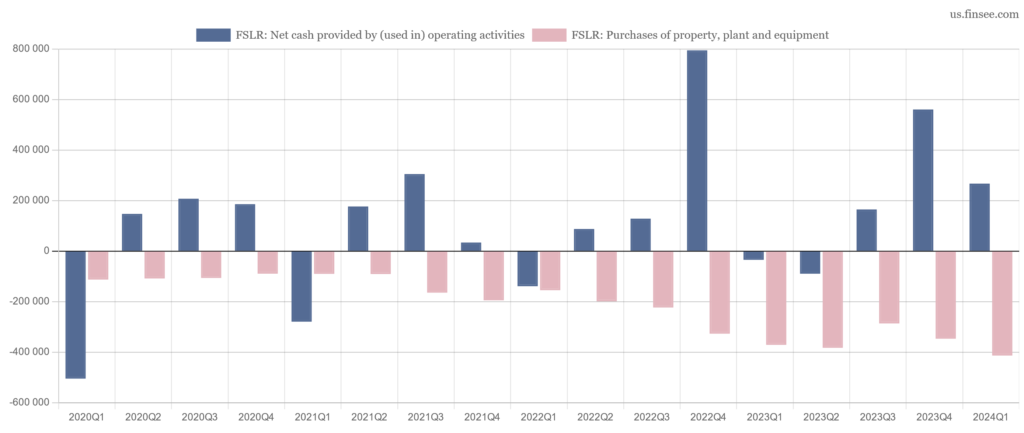

Cash Flow

Cash from operating activities is mostly enough for FSLR needs. It issues only small amounts of debt when needed

First Solar invests heavily in new plants and equipment. The majority of money comes from operating activities.

As a result, the company needs only small amounts of external financing, usually in the form of debt. It does not pay dividends or buy back significant amounts of shares.

Summary

First Solar is expected to show outstanding result in 2024. But our view is mixed: it can be a multi-bagger or it can stop growing fast enough.

A significant drop in new net-bookings adds risks to the company.

If they recover, First Solar is positioned extremely well to ride the wave of energy transition: there’s enough cash and enough backlog of orders. But if they do not, 2024 could be a peak.