Review date: December 18, 2024

All numbers on the charts are in millions of EUR, except when stated otherwise.

Verdict:

We think Nokian will be able to exceed pre-war (2021) sales and produce the same earnings in 2.5 years. As a result, shares could return to 2021 levels in spring 2027, bringing a 300% upside.

Pros:

- fast sales growth;

- dominating winter tire brand in the main market;

- 60% of the turnaround is finished with all milestones achieved on time and within the budget.

Cons:

- tire market is weak in 2024;

- new tire factory could have lower margins than the old one;

- Nokian had to sacrifice its market share in Central Europe and now needs to catch up.

Nokian manufactured the first winter tire 90 years ago and remains the market leader in Scandinavia due to its high quality.

Winter tires for passenger cars and trucks are the main product, Nokian also makes summer and all-season tires. Almost all sales come from the replacement market (drivers replacing tires on their cars), and only a small amount – from tires installed by car manufacturers.

Geographically the company sells its tires in Scandinavia and Iceland (Nordics), Canada and Northern US states (North America), and Central Europe (Other Europe). The total market share is approximately 2% in these markets. The company focuses on niche segments with high margins.

Nokian produces its tires in three plants: Nokia (Finland), Dayton (Tennessee, USA), and Oradea (Romania).

- The turnaround.

- The current state of the tires market.

- Financial situation.

- Summary

The turnaround

2.5 years have passed since Nokian launched its 5-year transformation plan. So far the company hit all milestones

In March 2022 Nokian decided to close its biggest plant located in Russia, as the full-scale Russia-Ukraine war started. This facility had three advantages: cheap energy, cheap labor, and proximity to the head office in Finland.

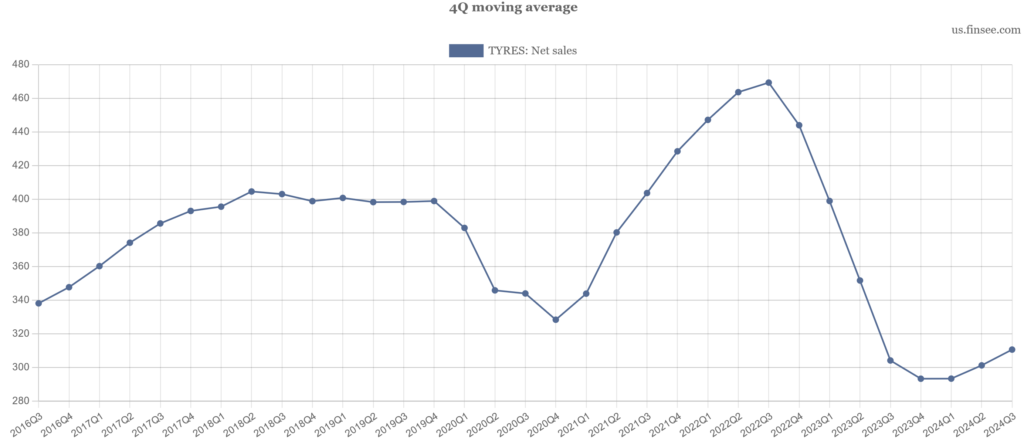

As a result, quarterly sales were down 37.5% after the company sold off the remaining tires in mid-2022 and Nokian’s share price plunged 80% from the pre-war level.

Sales are in million EUR, 4Q moving average:

The company made three big decisions.

1. Added manufacturing facilities:

expanded plant in Finland in 2023;

expanded plant in the USA in 2024, full capacity from 2025;

built a new zero CO2 plant in Romania. The first tire was produced in July 2024, production at scale will begin in early 2025, with full capacity from late 2026.

So far, everything has been finished on time and within the budget.

2. Signed contract manufacturers from China to fill in the temporary gap. The tires are made according to Nokian specifications and sold under the Nokian brand. The company made this arrangement permanent with more contract tires during peak demand periods and fewer during a downturn, with stable manufacturing at its own facilities.

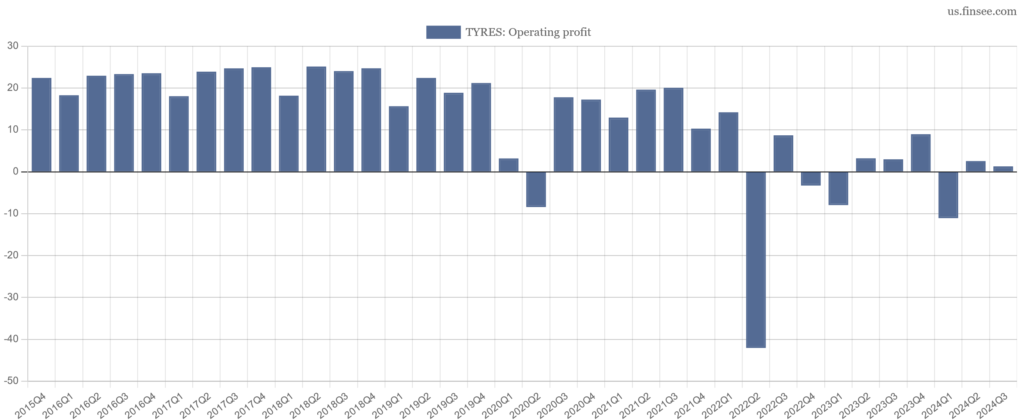

The operating profit margin suffered heavily, as these tires cost more (chart is in % of sales):

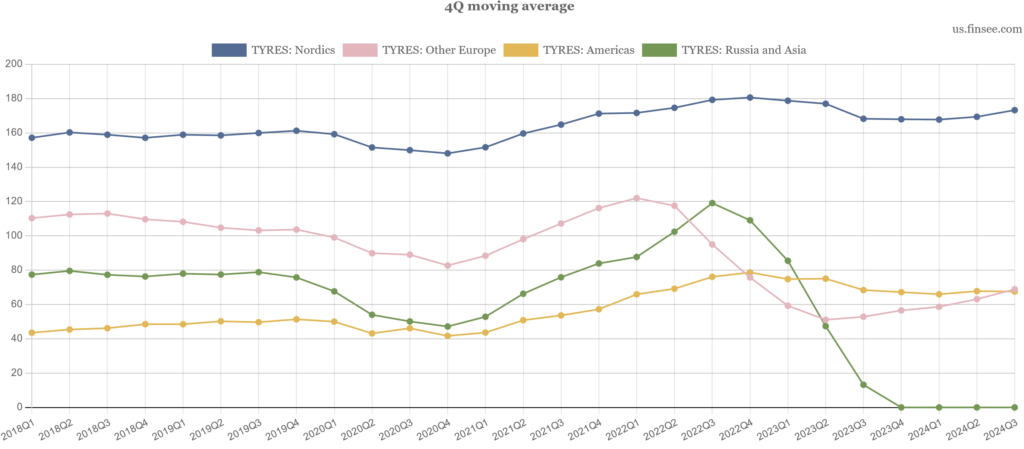

3. Maintained sales in Nordics and North America, sacrificing market share in Central Europe. Sales in Russia were stopped after the remaining inventory was depleted.

Numbers are in million EUR, 4Q moving average:

Nokian plans to achieve the following targets in 2027:

| Target | 2027 | 2021 |

| Sales, bln EUR | 2.0 | 1.7 |

| Operating margin | 15.0% | 15.6% |

| Tires produced, millions | 15.0* | 19.0 |

| Net debt / Ebitda ratio | 1.0-2.0 | -0.2 |

* in addition Nokian plans to sell tires from contract manufacturers.

The company is going to sell higher-priced tires with a bit lower operating margin in 2027. We expect the same net profit because of higher debt and lower operating margin.

Main factors, impacting operating margin:

Positive:

- Romania factory will employ 650 workers vs 1100 in Russia;

- SUV and EV sales increase demand for more expensive tires;

- the first zero CO2 tire factory opens the market of climate-conscious buyers.

Negative:

- higher energy costs in Romania;

- a higher share of all-season and summer tires (they are cheaper than winter tires).

Explanation of Nokian transformation from their 2023 Annual report:

The new CEO Paolo Pompei, 53, will lead the company from January 1, 2025. The current CEO Jukka Moisio, 63, decided to retire earlier this year.

According to the company’s statement, Pompei has “very strong international experience”, likely meaning that his main task would be a significant increase in sales beyond Scandinavia. His recent job was as President of Yokohama TWS, an Italy-based division of a leading Japanese tire manufacturer.

The current state of the tires market

sales continue to grow strongly in the main Nokian niche markets

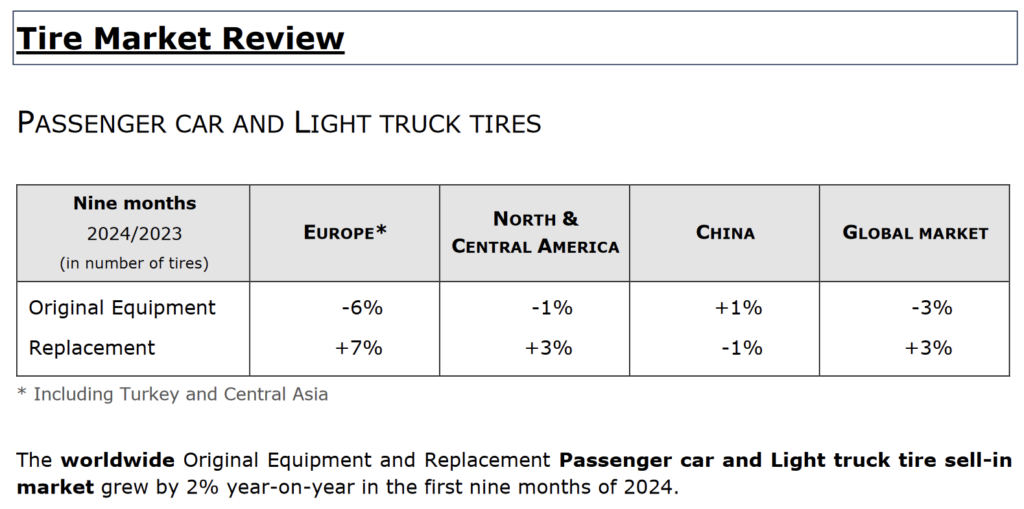

Overall tire sales are expected to be flat in the target regions. Nokian 2023 annual report:

According to Global Data, the demand for tires will grow moderately in Nokian Tyres’ primary markets during 2024–2027. The yearly growth rate is estimated to be approximately 2 percent in the Nordic countries and North America and approximately 1 percent in Central Europe.

The main reason is lower new car sales. As Nokian operates in the replacement market, it is positioned much better to tackle this weakness: drivers will continue replacing old tires. Only the first-year winter tire sales will suffer (new cars are usually equipped with summer tires in the target regions).

Michelin’s (one of the biggest Nokian competitors) Q3 2024 financial information confirms this point:

Competition intensifies as Chinese manufacturers flood European and American markets with cheap tires. But Nokian produces premium tires, not affected by competition from China yet.

Climate change in Central Europe and North America poses a significant threat to Nokian: more people buy all-season tires as winters become milder. Still, many governments demand that cars be equipped with winter tires from November till March. Also, drivers don’t have much choice in Nordics, Canada, and mountain regions: even if heavy snow and frost happen only 4-8 weeks per year, they need proper winter tires to handle it.

In addition, Nokian will further increase the production of all-season and summer tires. But it doesn’t have such a strong brand and pricing power in these segments.

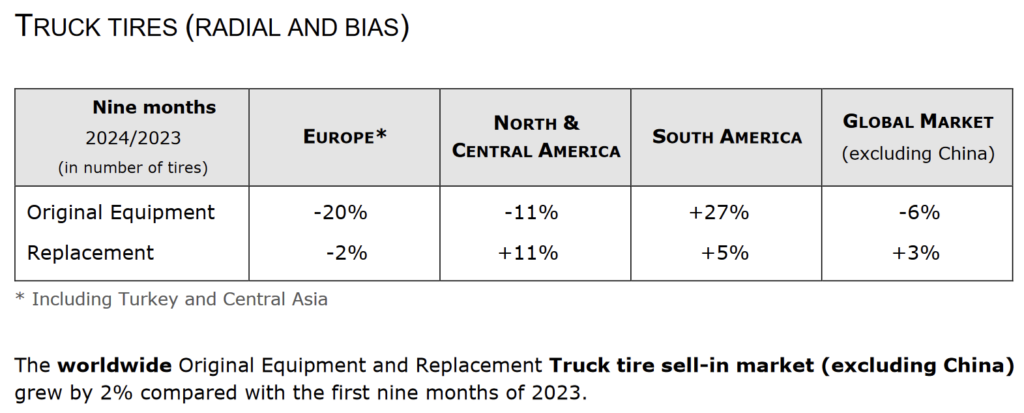

The heavy tires market “doesn’t look too promising when we are looking towards the year-end”, according to Nokian’s CFO. Still, Nokian sales in this segment were down only 3.0% YoY in Q3 2024, compared with a 10.8% YoY decline a quarter earlier. This segment represents 18.5% of the total Nokian sales.

Michelin’s earnings showed a similar YoY picture in truck tires: -4.6% sales and -5.5% volume for 9M 2024. Market data from Michelin’s Q3 2024 earnings:

Despite the overall weakness, premium tires continue to show strong growth. Michelin plans that 18”+ tires market will have a 12% Cagr in 2023-28. Pirelli estimates that 18”+ tire replacement market grew 7.5% YoY during 9M 2024, compared with a 0.5% growth for ≤17” replacement tires.

This is the result of higher sales of sport utility vehicles (SUVs) and electric vehicles (EVs). SUVs usually have bigger wheels than sedans or wagons. And EVs and hybrids are significantly heavier than petrol or diesel (ICE) cars, increasing demand for larger size and more expensive tires.

Even though EV sales are lower this year, they still replace old ICE cars. So the total number of EVs on the roads continues to rise significantly.

The new zero CO2 tire factory in Romania is the world-first and allows Nokian to enter a niche of climate-conscious buyers. Nokian has already signed an agreement with Polestar (Volvo’s sister company) to create a climate-neutral car by 2030.

Nokian will manufacture almost all US tires in the US factory: potential US import tariffs won’t impact the company.

Financial situation

sales are gradually returning to the 2021 level and the debt amount is moderate

We will not include charts and comments already discussed in the turnaround section.

Sales

Nokian needs to grow sales by 12.6% Cagr during the next 3 years to reach the 2021 revenue. In Q3 2024 they achieved 13.6% YoY growth, or 14.4% in comparable currency.

These numbers include a 5% negative impact on sales in Q3 because some summer tires arrived late due to the Red Sea shipping crisis and had to be discounted heavily.

The main growth driver for the next year is the new Romania factory, where a capacity for 3 million tires is already installed, according to the CFO. With more than half available for 2025, we estimate these tires will add 15% to the company’s sales in 2025 and at least 10% in 2026.

The second driver is full capacity in the USA factory next year but the management didn’t provide any numbers. In the Q2 earnings call the CEO said that in the USA Nokian is constrained by supply, not by demand: “we are basically able to sell everything we produce in Dayton“.

Yet in Q3 the talk on the earnings call was different. CFO said: “customers [in the USA] are moving to tier 3 and tier 4 [low-cost] tires”.

CEO added that the weather was warmer than usual: “you see a good momentum in North America, especially in Canada. The US is more weather-related. You see that it’s quite warm on the North American side. We had good pre-orders for the season, but, of course, the season to materialize required that all those pre-orders materialize. We need the season to start and the weather to change”.

After a 10.3% YoY growth in Q2, the USA sales were down 1.4% YoY in Q3. We think this is the main reason why Nokian shares traded lower after the Q3 earnings. If the company increases manufacturing but is unable to improve sales, Nokian could be in big trouble: higher depreciation and debt load could depress earnings for years to come.

On the other hand, USA sales dynamics go zig-zag each quarter, so we’ll watch closely the Q4 numbers here:

The heavy tires segment (18.5% of total sales) also shows weakness with the CFO commenting during Q3 call: “sales are decreasing and that’s mainly due to the weak OEM [original manufacturers – tires on new vehicles] market. I think we have visibility, but it doesn’t look too promising when we are looking towards the year-end”.

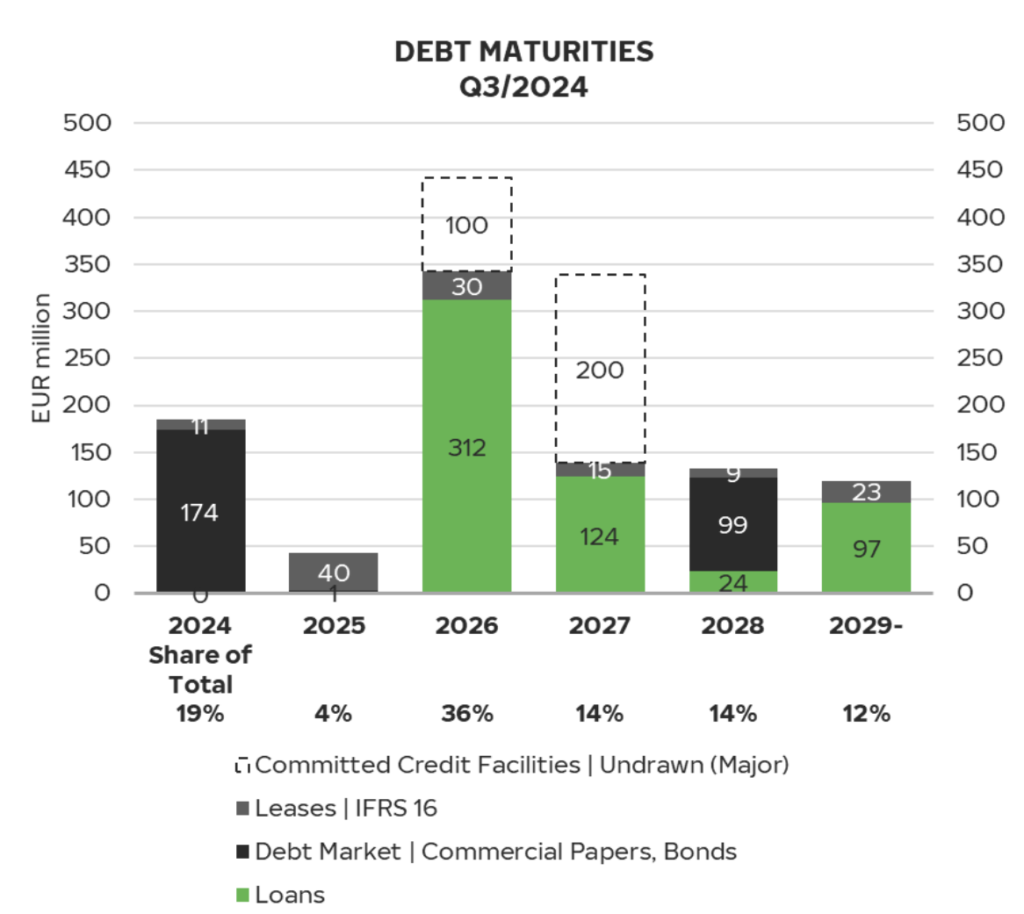

Debt level and cash flow

The CEO said that net debt peaked in Q3 2024 at 801 mln EUR, which is likely true. Nokian needs to invest 100 mln EUR more in the Romania factory in Q4, which will be offset by 300-350 mln EUR operating cash flow in Q4 due to the seasonality:

Next year they will need to invest the final 200 mln EUR in Romania and will start receiving a 99.5 mln EUR government grant for building the factory. We also expect a better operating cash flow in Q1-Q3 2025 because Nokian will produce more tires in its factories, improving margin.

The debt repayment schedule is manageable: the company is expected to repay 225 mln EUR and invest 300 mln in the next 5 quarters, with 160 mln in cash, 300 mln in committed credit facilities, and 400-500 mln in operating cash flow.

We forecast Nokian will generate 400 mln EUR in operating cash flow in 2026 to pay 342 mln in debt. The chart is from the Q3 presentation:

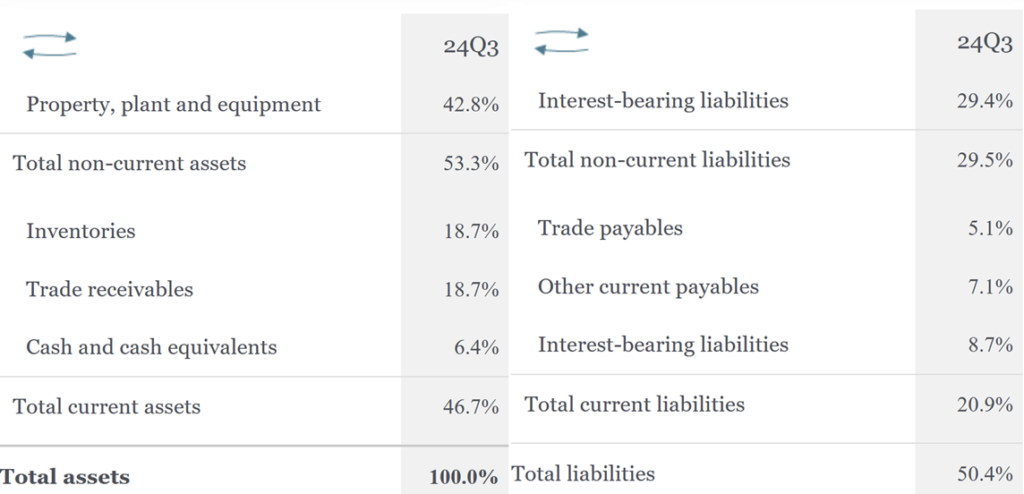

Balance sheet

The balance sheet is solid with current assets covering almost all liabilities. Usually, half of the receivables turn into cash in Q4. The numbers are in percentages of total assets, only articles with 5%+ of the total are included:

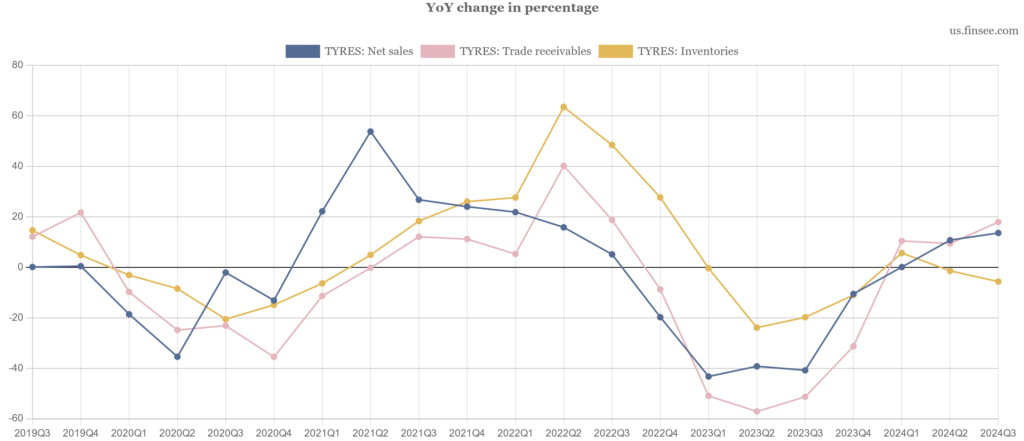

Receivables grew 17.9% YoY in Q3 2024, with one analyst asking for the reason for such a spike during the call. The CFO said this is the usual business and we agree with this statement: a year ago they were at an extremely low level. This year receivables grew at the same pace as sales. Inventories even went down:

Summary

We think the chances are very high that Nokian will succeed in its 5-year turnaround plan with a 300% potential upside for the share price in 2.5 years, or 74% IRR as it could return to the pre-war level.

With new manufacturing capacity Nokian could expect a 15-20% sales growth for the next 3 years, enough to reach a 2 bln EUR sales target for 2027. Margins will also improve because internal manufacturing has higher margins than contract manufacturing from China. It is also much closer to the main markets with a low risk of shipping disruptions, which had a 5% negative impact on revenue in Q3.

Made-in-China contract tires will likely represent 20% of future sales, allowing Nokian to fully utilise its factories by providing a necessary cushion in times of high demand.

As Nokian returns its manufacturing capacity to the market, the main question is: will the customers return to the brand?

We think the answer is positive because Nokian has a strong position in a highly profitable and growing niche of the tire market. We expect SUVs and EVs market share to improve further in the coming years, increasing demand for premium tires. Nokian plans to sell a bit fewer tires at a higher price and SUVs and EVs will likely allow the company to achieve this goal.

Nokian sacrificed the Central European market in 2022 and this year sales are growing at 30-35% YoY in this region, demonstrating that customers return to the trusted brand as soon as they have Nokian tires available, even if they are currently made in China. Still, Central Europe has a lot of room to catch up with 9M 2024 sales down 38% from 3 years ago. North American sales are up 21% and Scandinavia is up 1% during the same period.

The main risk in our opinion is climate change with customers choosing all-season tires more often instead of winter ones. US sales in Q3 highlighted this trend with warm weather delaying customer purchases. We think this risk is mitigated at least for the next decade as severe winter weather is still common in the main Nokian markets, even if now it is 4-8 weeks, instead of the 8-12 weeks a few decades ago. We will watch North American sales closely in the coming quarter to check for this risk.

The company plans to manufacture more all-season and summer tires in the future but the Nokian brand is not as strong in these segments.

We bought Nokian shares in our portfolio as, in our opinion, the opportunities far outweigh the risks.