Review date: June 26, 2024

All numbers on charts are in thousands USD, except when stated otherwise.

Verdict:

Unity is a buy for us as a high-risk / high-reward investment. The company is in the middle of a transformation, which could turn things around starting from H2 2024.

Pros:

- dominating position in mobile games and virtual reality;

- interim management did many right things during the last 6 months.

Cons:

- customer backlash from ousted CEO’s decisions;

- new CEO hasn’t shared his vision yet;

- high share dilution.

- The problem.

- Competition in Gaming and VR.

- Competition in Mobile Ads.

- Transformation.

- New CEO.

- Financial situation.

- Our long-term vision for Unity.

- Summary.

- Footnotes.

The problem

Unity shares are down 92% from the peak $201.12 in November 2021 to $16.09 in June 2024

The previous management did many things wrong:

- spent $5.1B on multiple acquisitions in 2021-22, most of them paid in stock, and many already sold or written down in the recent reorganisation;

- issued huge amounts of shares for employees;

- presented new versions of software each year with many bugs;

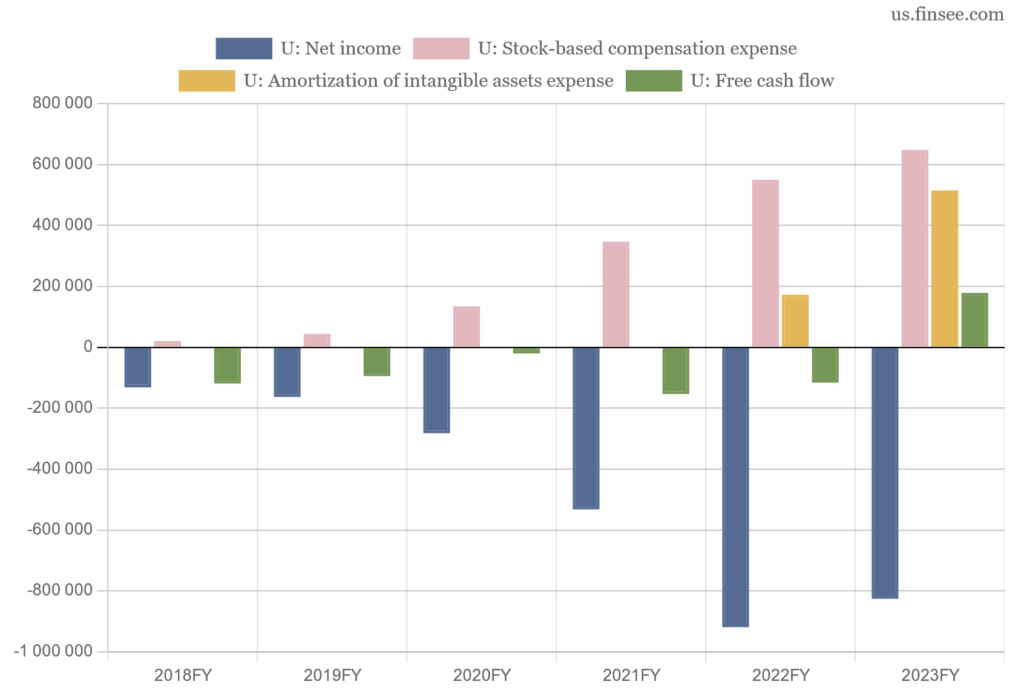

- had $919M and $826M net loss in 2022 and 2023;

- tried to remedy the situation by charging a fee for each game install above a certain threshold, which infuriated many developers and triggered CEO’s firing.

As a result, the following changes happened in financial reports between December 31, 2020 and December 31, 2023:

- diluted shares went up 115% from 220.8k to 475.4k;

- debt increased from virtually zero to $2.2B;

- cash decreased by $100M.

Despite serious net loss Unity was free cash flow positive in 2023, because the largest expenses are non-cash: stock-based compensation and amortisation of intangibles.

The company is not heading to bankruptcy right now but the problem is – it cannot return money to shareholders.

Unity expects to issue 18.2M or 3.8% more diluted shares during 2024. This is a much lower number than before but still too much for a 20-year-old company. Some are a part of restructuring, others belong to the new CEO. However, there was no explanation from the CFO for the majority of these shares during the Q1 2024 earnings call. Maybe they will go to the new management team, which the new CEO will bring with him.

Competition in Gaming and Virtual Reality

Unity is in a strong position to dominate mobile games and VR development markets as a light-weight but powerful engine

The main competitor of Unity in this segment is Unreal Engine developed by Epic Games. Epic Games is still a private company so the numbers are not precise:

| Share of developers | Unity | Unreal |

| Primary engine for mobile games | 38% | 15% |

| Total use of the engine in mobile games | 70% | 43% |

| Engine for VR development | 62% | 12% |

They are comparable in characteristics but serve different purposes, making a small monopoly for each engine in their niches:

| Difference | Unity | Unreal |

| Games visual quality | Any 2D or 3D | Mid or top 3D |

| Hardware demands | Low to high | High |

| Learning curve for developers | Medium | High |

| Developer community help | High | Medium |

| Plugins | Allows third-party | Only Unreal’s |

Lower hardware demands make Unity a perfect choice for most mobile and VR games and development. This becomes a critical advantage as Apple decided to launch a cheaper VR headset in the future because sales of the $3500 Vision Pro didn’t meet expectations.

Reddit user on the difference for mobile and PC:

Our studio uses both Unity and Unreal. Unity are great for making non-shooter mobile games, and Unreal is great for making PC games and shooter games for all platforms.

…we love C# [language used in Unity] over C++ and we have a ton of Unity assets for mobile. Unity allows custom import script that batch optimizes assets for each platform too, so we can trim down our mobile games really really small, automatically.

Unreal … is a cutting-edge game engine especially for PC platform … with the support of Nanite, Lumen, Ray-tracing, DLSS 3.5 and a lot more that Unity doesn’t even have on its roadmap.

Also, novice developers are more likely to use Unity. They often lack knowledge to code in a more demanding programming language used in Unreal and need more community support.

This creates a self-reinforcing cycle: new developers begin to use Unity and as they become experts, they have less incentive to switch. As more developers use Unity, its community support improves, creating a higher incentive for novice developers to begin with Unity.

Reddit user summed up the difficulty of Unreal for novices:

I used and loved Unity for a long time and I struggled to get anywhere with Unreal many times so I feel uniquely qualified to answer this question!

There is a lot less to “figure out” in Unity.

In Unity, it’s pretty much just GameObjects, Components, Prefabs, and the lightbulbs start to turn on, and you can imagine making any game with just those tools. But in Unreal, there are systems within systems within systems, and tons of options everywhere, and way more types of classes that are similar to each other, and blueprints, and pages and pages of useless fields, and it’s all very overwhelming to me.

Another Unity competitor in game development is the open-source engine Godot. Currently, its market share is tiny but Godot could become a risk for Unity with the 2023 Unity’s price debacle.

A lot will depend on the features and pricing of the new Unity 6 engine and the new CEO’s ability to calm down game developers.

Whether Godot used its chance to pose a serious threat to Unity remains an open question as games take many months and sometimes years to develop. We’ll have a more clear picture in 2025.

We consider this risk as medium because Godot has a chicken and egg problem: in order to have more games you need more Godot developers and better third-party support and in order to have more developers and support you need more Godot games shipped to market.

A search on Indeed returned 270 jobs for “unity developer” (a few of them from Unity) in the USA vs just 4 jobs for “godot developer” on June 23, 2024.

The difference on Upwork was 281 “unity developer” vs 22 “godot developer” jobs.

Competition in Mobile Ads

Unity is well-positioned to regain ground: its game engine strength could significantly improve ads sales

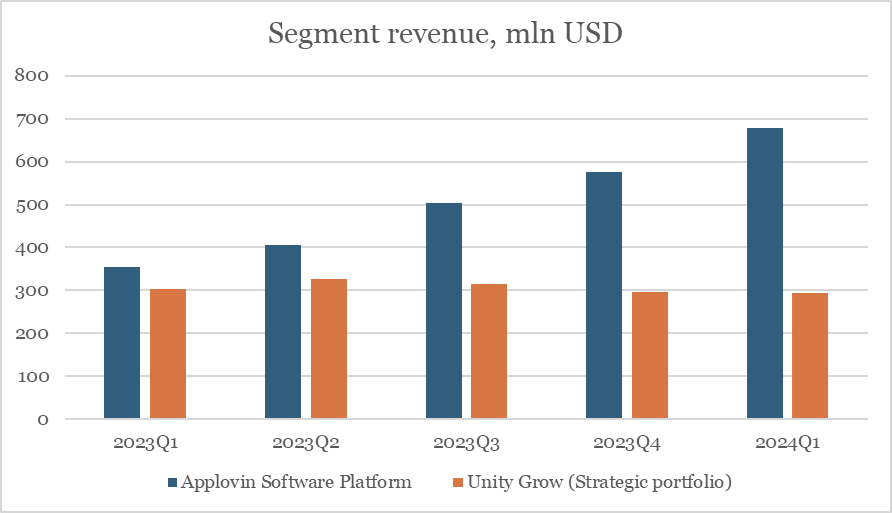

Since the ironSource acquisition in 2022 Unity has 60-65% of its revenue as an Ads marketplace in mobile applications, this market has a few big players with AppLovin becoming the biggest threat recently.

Both companies’ revenue from Ads was pretty close in Q1 2023 but during the last year AppLovin made a breakthrough. Note that Unity’s revenue includes only the Strategic portfolio – parts of the business that Unity will keep after the reorganisation:

Some would consider this an insurmountable lead but we think that Unity has a potent tool to turn things around: its next Unity 6 game engine.

Unity’s previous CEO John Riccitiello made a bold attempt at forcing Unity developers to use Unity ads for their games, which failed with other pricing innovations. But now Unity’s management has a different approach: previous Unity versions will have the same pricing as before, only the new version will have new pricing. If you want the most modern tools, pay directly or use Unity Ads in your games.

This is based on the comment of then-interim CEO Jim Whitehurst during the Q1 2024 earnings call:

And whether that revenue source is, I’ll call it, direct kind of pay us based on usage or indirect, use our monetization, our ad stack, and therefore we get some degree of monetization on that, I don’t really care, right?

But I think the key is for us to be able to continue to invest and build the runtime to be extraordinary and long-lived … We need the revenue stream. And again, whether it’s direct or indirect, I don’t think we

care as much.

If AppLovin provides only ads solution but Unity provides ads solution and the most popular game engine combined, why not use Unity Ads?

AppLovin’s Ads success in 2023 shows how big and profitable (73% adjusted Ebitda) this market is.

AppLovin tried to eliminate this threat by offering $20B to buy Unity in 2022. There were also rumors about a potential $17.5B bid in 2023 after the Unity pricing debacle.

Transformation

Unity has almost finished its transformation, concentrating on core segments and significantly reducing costs

In H2 2023 Unity fired its CEO John Riccitiello and hired an interim CEO Jim Whitehurst, who cleaned the business:

- sold or closed non-core businesses with high costs and low revenue, concentrating on the Game Engine, Cloud, Ads, and 3D solutions for enterprise customers;

- reduced workforce by 25%;

- made other savings like cloud hosting, offices, and software licenses.

This process mostly finished in Q1 2024 with the following annual impact for earnings:

| Impact, USD | |

| Revenue ex-one-off items | -283M |

| Operating expenses, ex-stock-based compensation | -250M |

In addition, there would be savings in cost of goods sold and stock-based compensation expense. These actions improved quarterly adjusted Ebitda by $50M from $29M in Q1 2023 to $79M a year later. For 2024 Adjusted Ebitda for the Strategic portfolio (remaining businesses) is guided to increase 51% YoY to $412.5M.

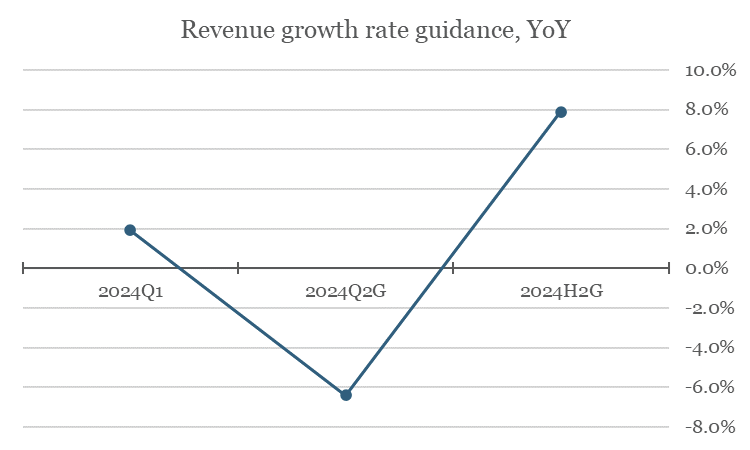

Guidance for the Strategic portfolio revenue:

Unity beat Q1 2024 revenue guidance by 1.9% (it was expected to be flat) but forecasts Q2 sales to fall 6.4% and H2 to rise 7.9% YoY. During the Q1 2024 earnings call then-interim CEO didn’t provide a lot of specifics about growth drivers. He said that a number of initiatives were started in January 2024 which will boost results from August.

The date of the Unity 6 release is not disclosed yet.

During Q2 2024 the company plans to invest in cloud consumption to drive more data and data scientists because “that just pays out very quickly”. This puts pressure on Unity’s adjusted Ebitda for this quarter, which is guided to remain almost flat QoQ.

Industry segment

This is the fastest-growing segment of Unity: companies can create their own 3D experiences to train employees, show their work to customers, present themselves to investors, and many other applications.

Interim CEO saw a bigger opportunity in the Industry in the long run than even in the Games.

Unity sold part of this business to Capgemini in April 2024. The statement was vague but based on the management’s comments in the earning calls, we can assume that Unity has the software part of this business and sold the application part. X thread discussing this transaction in more detail.

To make an analogy this would be like if Google sold its Pixel phones manufacturing but kept the Android platform in-house so other phone manufacturers could build on it.

We think this is the correct approach because Unity concentrates on its core strength: making the top 3D engine. Each Industry customer needs a bespoke solution, like in the Games segment, where Unity doesn’t create games. Individual solutions is the area of expertise of consulting companies, like Capgemini, and in our opinion creating the engine used by many, is a much more lucrative business.

New CEO

Mathew Bromberg has relevant experience in turning around a company in the gaming industry

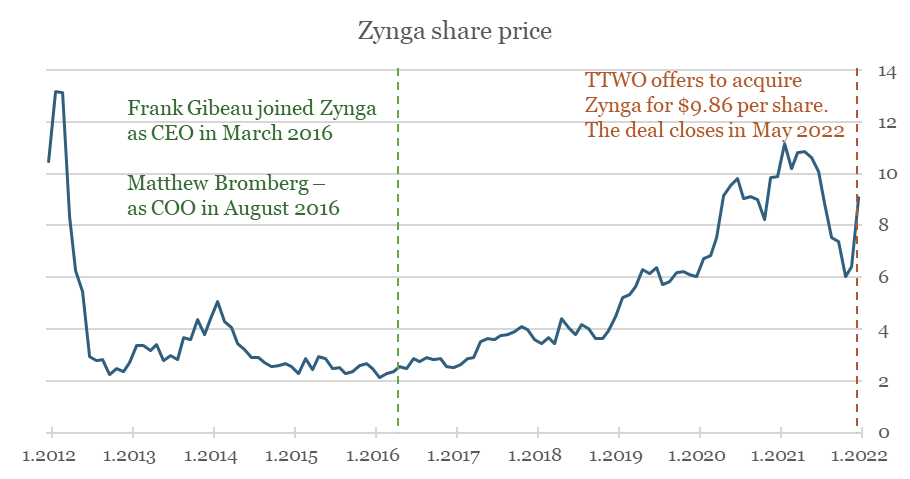

In May 2024 Unity hired new CEO Matthew Bromberg, 51, who took part in game developer Zynga’s successful turnaround as Chief Operating Officer in 2016-2022.

Zynga’s revenue grew with 30% CAGR during those 5 years:

| 2016FY | 2021FY | CAGR | |

| Revenue | 741.4M | 2800.5M | 30.4% |

| Operating income | -114.2M | 55.8M | |

| Operating margin | -15.4% | 2.0% | |

| Net Income | -108.2M | -104.2M | |

| Net margin | -14.6% | -3.7% | |

| Free Cash Flow | 49.7M | 241.3M | 37.2% |

This was achieved by two main changes: choosing better acquisition targets and giving studios more freedom to develop hit games. Note that all big game developers actively acquired smaller competitors during this time. It wasn’t a question of whether you need to pursue M&A but which company to buy to stay ahead. In 2022 Zynga itself was acquired by Take-Two Interactive for $12.7B.

Unity has a different situation with low shareholder appetite for new acquisitions, yet Matthew Bromberg’s experience in Zynga is very relevant for both main Unity segments:

1. Zynga was one of the biggest game developers using Unity’s game engine.

2. Zynga created its advertising marketplace with $551M in sales in 2021.

Mr. Bromberg hasn’t shared his vision for Unity yet. However, we can assume it wouldn’t be too different from the interim CEO Jim Whitehurst’s transformation: he hired Bromberg and became Unity’s Executive Chair.

Financial situation

Unity has stable financial position and in our opinion would be able to generate enough cash to be an attractive investment at the current share price

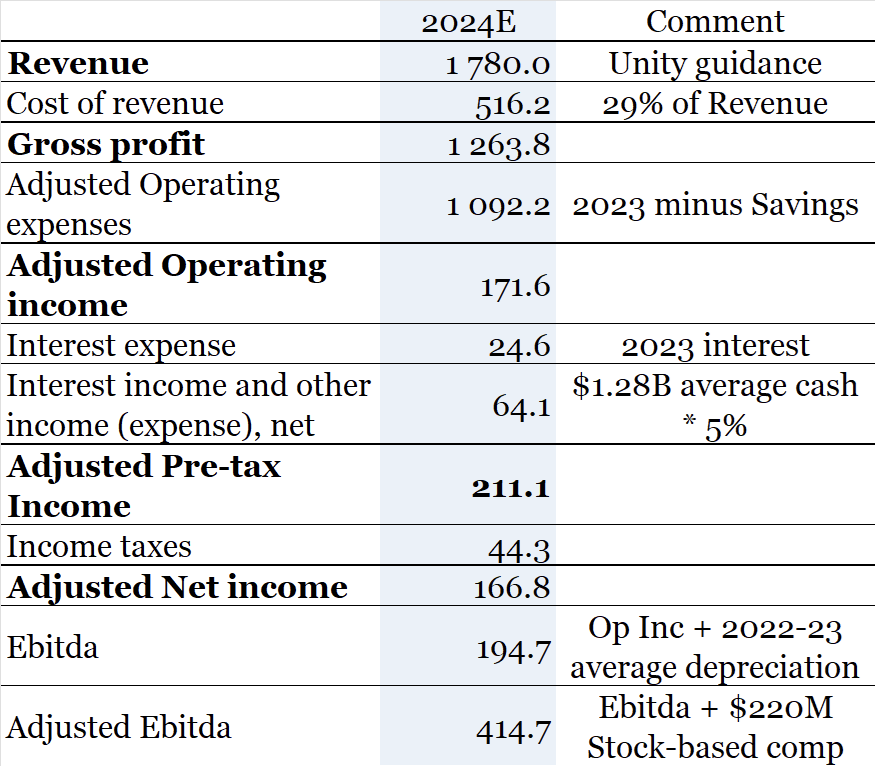

Recent Unity financial reports include many redundant activities and one-off operations. So we made “clean” model financial statements for 2024 based on Unity’s guidance and our calculations.

Warning:

Our calculations below are non-GAAP and could be wrong

Income statement

We made following assumptions:

- Cost of goods sold (COGS) – as Unity got rid of the recent unprofitable acquisitions, we expect it to go down 4.5 percentage points to 29% of revenue;

- Share-based compensation (SBC) – calculated at the current Unity share price, instead of much higher 2020-23 prices used by GAAP measures;

- Amortisation of intangibles – calculated as zero because in Unity’s case, we think this amortisation is counted twice: in operating expenses to replenish these assets and then separately as amortisation;

- Operating expense (OpEx), ex-SBC and ex-amortisation – we included savings of $250M, according to Unity’s guidance.

Detailed explanations are in the footnotes.

We arrived at the following Operating Expense savings, in millions USD:

| 2024 estimate | Savings, compared to 2023 | |

| Adjusted Share-based compensation | 220.0 | 428.7 |

| Adjusted Amortisation of intangibles | 0.0 | 515.5 |

| Other OpEx | 870.2 | 250.0 |

| Total Adjusted OpEx | 1 092.2 | 1 194.2 |

Our model non-GAAP Unity Income statement for Strategic Portfolio, in millions USD:

With added amortisation of intangibles and share-based compensation at 2020-23 stock prices, we expect $285M GAAP Net loss for 2024 Strategic portfolio.

Both main expense items for 2023 will go down significantly in the following years:

Stock-based compensation – because the share price fell 92% from its peak in 2021 and later compensation packages will be counted at the current price. Also, we expect fewer new shares to be issued as the market is closely watching this metric and Unity reduced its workforce by 25% recently.

Amortisation of intangibles – because they will be amortised in 3-6 years and Unity doesn’t plan big acquisitions for the near future. It is expected to go down from $515M in 2023 to $352M in 2024 and $167M in 2027.

This is why we consider our adjusted Net income as a better approximation of the current earnings power of Unity.

Cash flow

Free cash flow calculation for Strategic portfolio, in millions USD:

| 2024E | |

| Adjusted Net income | 166.8 |

| Income tax (compensated by deferred tax assets) | 44.3 |

| Stock-based compensation | 220.0 |

| Depreciation | 48.4 |

| Purchases of property & equipment | -55.9 |

| Free cash flow | 423.6 |

With the market cap of $6.5B, this estimate equals to Price to Free Cash Flow ratio of 15.4, which we consider attractive for a company with such a strong competitive position in a potentially breakthrough VR segment.

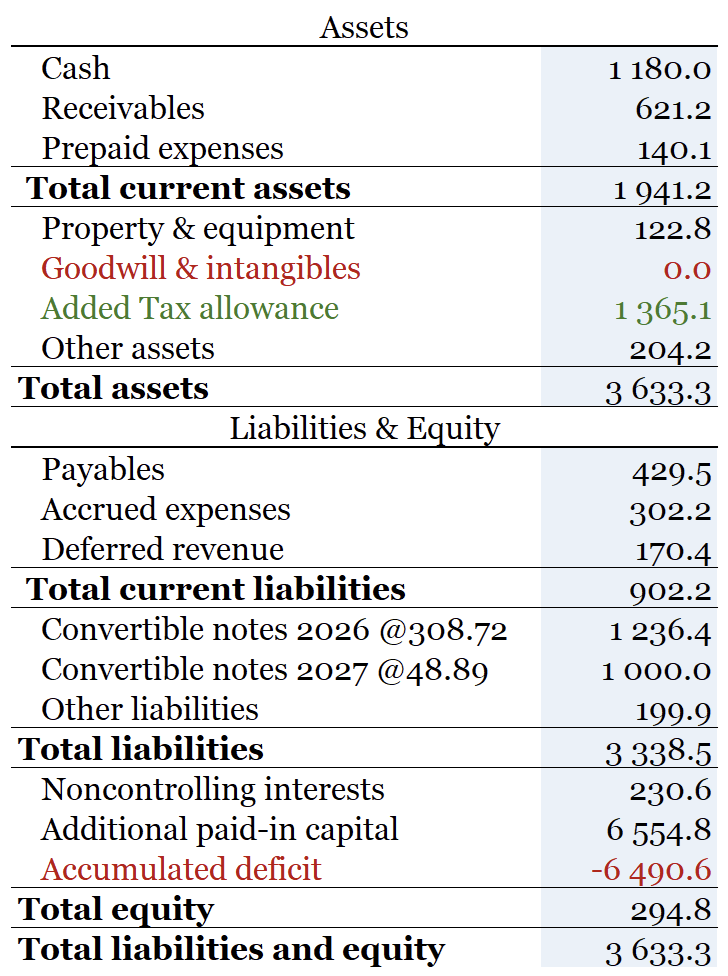

Balance sheet

To make a “clean” balance sheet we:

- removed $3.1B of Goodwill and $1.3B of Intangibles;

- added back $1.4B of Tax allowance (including $0.3B from writing down of Intangibles) as we expect that Unity will become profitable in the following years and will add these Deferred tax assets back on its Balance sheet – details;

- increased Accumulated deficit by $3.0B to balance the first two changes.

Simplified non-GAAP Unity Balance sheet, March 31, 2024:

Unity has a stable financial position with 2026 Convertible notes covered by cash and more than three years before 2027 Convertible notes mature. If our estimate of $424M of free cash flow for 2024 is correct, Unity could generate more than enough cash to pay these notes. Management expects an Adjusted Ebitda of $413M in 2024, which correlates with free cash flow.

Our long-term vision for Unity

Unity has the perfect platform for some revolutions happenning rigth now

Warning:

This is our view of the future potential. Unity’s transformation could fail, better technology could emerge, consumer habits could change, and many other risks to consider.

1. Game development becomes more and more democratised. Then-CEO of Zynga Frank Gibeau told the FT in 2021:

The rise of mobile gaming was causing “tectonic changes” in the industry as small budget teams can leverage graphics engines from gaming development groups Unity and Unreal, computing power from Amazon Web Services, and high-performance internet from 5G, and then compete for attention with some of the biggest companies in the world.

“When I was doing this 10 years ago at EA (Electronic Arts) you would have to spend hundreds of millions of dollars in tech development tool and infrastructure to make that happen,” Gibeau said. “Now, because the tools are so darn good, very small companies can get in. The barrier to entry into these things has really dropped dramatically.”

With people having more and more free time (four-day working week, more retirees each year) there will be more and more game creators and game consumers. The payout for game creators is much better than for YouTube bloggers: a successful game will bring money for many years, potentially even billions of USD.

As it becomes easier to create games, we expect more people to try themselves in this area than as a professional blogger on Instagram or TikTok. Creating your own successful game is a childhood dream comes true: other people play by your rules! And what’s better: you are not limited by the real world like on social media, where bloggers visit the same places and do the same things, you can create any worlds in the past, present, or future.

Unity could become the biggest winner from this trend: its game engine is the most popular among novice developers.

2. Combining its Game engine with Ads could dramatically improve Unity’s sales and earnings.

Beginning from the new Unity 6 version game developers will likely face the following choice:

- use basic or old tools for free;

- agree to put Unity Ads in a game to access advanced tools;

- pay money to access advanced tools.

We think most people will choose the second option as future game success is not guaranteed and many new developers lack money.

As a result, Unity Ads has a good chance to dominate the mobile and VR games advertising segments.

3. Industrial solutions have a lot of potential.

Unity Industries segment serves companies that create 3D solutions for their customers, employees, and investors. With huge improvements in VR headsets, there are multiple new opportunities:

- visualising new design in your house when you want to remodel it;

- allowing surgeons to practice in safe 3D simulations;

- helping factory workers to learn new equipment before it arrives;

- showing investors how your prototype will look and work.

This technology is already successfully used in military aviation, where traditional pilot training is too long and expensive. As US Maj. Gen. Craig Wills said in March 2021 :

The simulator-heavy experiment now halves the length of the current T-1 course to roughly 12 weeks within the training program, accelerating a pilot’s path to graduation.

Students learn general aviation foundation skills in the classroom and then head straight into the [next training stage], finishing in roughly seven months time instead of the traditional 12 months.

As VR software and hardware costs go down, we expect a huge interest from many industries. Learning by acting in a safe environment allowed us to get new skills fast when we were kids, this is the natural way instead of lectures in the classroom.

4. We think for the next decades AI is not a threat but an amplifier of Unity’s capabilities.

Humans closely working with AI achieve much more than AI trying to do things by itself.

Watch this video, created by the Unity team in March 2022:

What makes this video so special is that a model was created based on a real person with all tiny details and imperfections, which tricks our minds into thinking this is a real actress. We believe this is the future: models of real people, dresses, and furniture will be used by developers to create real-life-looking games and videos.

Many of the best books and paintings were created based on real people, who were put in different circumstances. Humans will make sure everything feels real, AI will make sure everything is developed faster and cheaper.

Unity is in a strong position to be the platform where this will happen, especially as it has a lot of experience with third-party plugins.

It took the internet more than 25 years from the first browsers to the Covid pandemic to dominate the world. Even now Walmart, Costco, and many specialised retailers compete successfully with Amazon.

We think the same will happen with AI: gradual removal of the border between what humans do and what AI does. And that specialisation will matter: a proper game engine will outcompete general AI solution in game development.

Right now AI is still at this stage:

Summary

At a 15.4 Price to Free Cash Flow ratio Unity is a buy for us. The company has a huge upside potential, coupled with big risks.

This is why we plan to hold it long-term or until there are material bad news.

We are going to watch closely during the next few months:

- how is the new Unity 6 engine received;

- is the new CEO’s vision for the future the same as ours;

- will Unity game engine lose market share to Unreal or Godot;

- does the company maintain its 8% growth target for H2 2024 and what is the target for 2025;

- will a 3.8% share dilution in 2024 be the last such big dilution.

Footnotes

Share-based compensation

We used two methods to count the current fair value of stock-based compensation, using $16.09 per share.

1. By counting vested and exercised stocks and options in 2023:

| Vested or exercised in 2023 | Units | Current value, $M |

| Restricted Stock | 11955677 | 192.4 |

| Employee stock purchase plan | 1064463 | 17.1 |

| Options ($9.42 average) | 5177930 | 34.5 |

| Proceeds from employee equity plans | -76.0 | |

| Total | 18198070 | 168.0 |

2. By counting new diluted shares in 2024:

| Units, 000 | |

| Diluted shares Jan 1, 2024 | 475373 |

| Convertible bond repayment | -1554 |

| Diluted shares Dec 31, 2024 (guidance) | 492000 |

| New shares | 18181 |

| Total value of new shares, $M | 292.5 |

| Proceeds from employee equity plans (2023), $M | -35.1 |

| New shares value, $M | 257.4 |

As the 2024 value is much higher, we took it as the base case. Not all shares will be vested and not all options will be exercised, that’s why we estimate the real value at $220.0M or 85% of the total new diluted shares.

Amortisation of intangible assets

We consider this expense as zero, because we think in Unity’s case this amortisation is counted twice.

All intangibles from sold or written-off businesses have been cleaned from the balance sheet. So only the active ones remain. They include the following values:

- $925M of Developed technology;

- $415M of Customer relationships;

- $67M of Trademarks.

Unity continues to develop new technology and expand customer relationships, which are already included in Operating expenses as R&D and Marketing, like with every other company. And then amortisation of old technology and customer relationships is also separately counted in Operating expenses, which is the case for companies that acquired many businesses.

To make an example, if a company has 5 cars $40k each with 5 years of useful life, and buys one new car per year to replace the old one:

| Calculations | |

| Number of cars currently used | 5 |

| Total value of cars | $200k ($40k price * 5 cars) |

| Useful life | 5 years |

| Depreciation expense per year | $40k ($200k / 5 years) |

| Cash used for buying a new car per year | $40k (price of 1 car) |

GAAP (US accounting standard) will consider $40k as an annual expense for this company. But with Unity’s intangibles it’s $80k – a depreciation of the old car and buying a new car combined.

Deferred tax assets

We added back $1.4B of deferred tax assets to Unity’s Balance sheet because we expect the company to become profitable again. The logic is:

Unity had $1336.8M of Gross deferred tax assets on March 31, 2024. These are income taxes, which are not needed to be paid because the company had losses in prior years.

For example, if a company began operations in 2022 and had a Net loss in 2022 of $200k and a Net income in 2023 of $250k, it will pay corporate tax only on $50k of income ($250k of profit minus $200k of the previous loss).

So its Deferred tax asset at the end of 2022 is going to be $42k (21% tax rate * $200k).

But Unity also created a tax valuation allowance of $1.088.2M, which is like depreciation for Property and equipment – it decreases the value of Tax assets. The reason is that Unity has remained unprofitable for many years and management does not expect to use these Deferred tax assets anytime soon.

But when the company turns profitable, which we expect will happen in 2-3 years, it will be able to add this allowance back to the Balance sheet, like Amazon did in 2017 or Tesla in 2023.

Unity has $1318.8M of Intangible assets on its Balance sheet. We removed these assets to look at the “clean” Balance sheet without Goodwill and Intangibles. This adds $276.9M to Deferred tax assets ($1318.8M * 21% tax rate).

The total addition to Deferred tax assets is $1365.1M ($1.088.2M + $276.9M).