Review date: May 28, 2024

All numbers on charts are in millions USD, except when stated otherwise.

Verdict:

ZoomInfo is a buy for us. Sales are slowing down, but we think this trend will stop in mid-2024 and ZI has the potential to benefit heavily from AI.

Pros:

- leader in the niche where AI could bring a lot of monetisable value;

- management claims that feedback from beta AI users has been overwhelmingly positive;

- forward PE ratio = 13.

Cons:

- sales growth is falling and is expected to fall at least until Q2 2024;

- many smaller customers are not renewing their subscriptions.

How ZoomInfo could benefit from AI?

ZoomInfo helps companies to find and convert prospective customers. ZI uses its database and algorithms to identify whom and when to contact to sell more.

In our opinion, it is the perfect niche for AI disruption, because AI could better analyse big amounts of data and find better prospects to contact. At the same time hallucinations are not an issue, because sales people are used to deal with prospects who don’t answer the phone or are not interested in the product.

For example, Chris is a sales rep. Right now out of 100 calls he makes, he could get 20 responses, 5 of them are interested in his offer, and 1 will become a customer.

With AI the numbers could be: 100 calls, 30 responses, 10 interested, 2 sales. Even if AI hallucinations led to 5 responses from people in unrelated fields, Chris would lose little time talking to them.

During Q1 2024 earnings call Zoominfo CEO said that beta users of ZoomInfo AI Copilot saved 10 hours per week for research and manual tasks and created nearly twice as many opportunities as similar non-users of beta AI.

ZoomInfo has a good position to benefit from AI tools, because of its proprietary database and direct impact on customer sales.

Segments

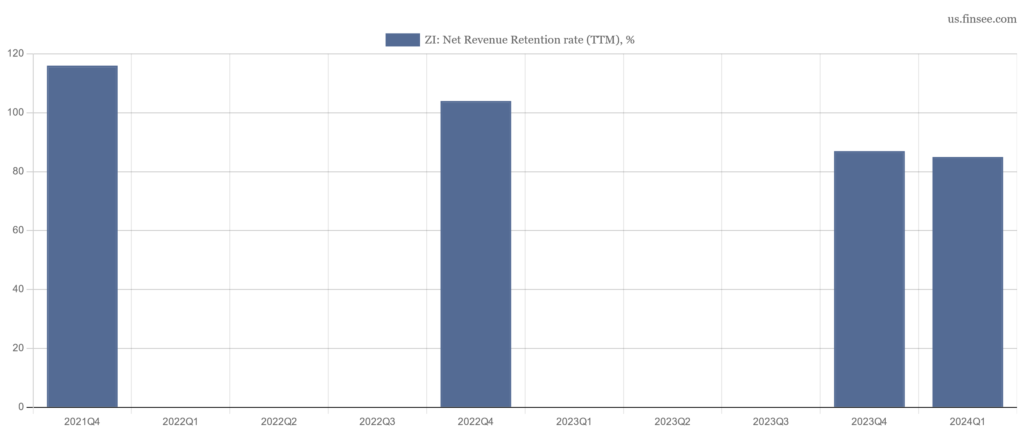

revenue from larger customers started growing after weak 2023 but retention of smaller firms fell

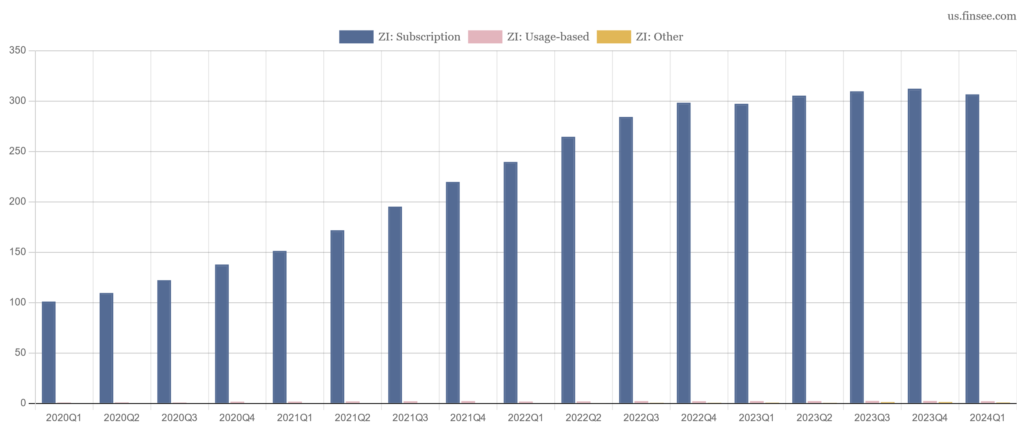

ZoomInfo reports sales by three service offerings but it is not very informative, because 99% of sales come from one offering: Subscription, with $300M+ sales per quarter.

The company also has other internal metrics, not shared in financial reports. During the last earnings call, CFO said that retention among the largest customers has stabilised in 2023 and started to improve in Q1 2024. Smaller customers began to feel more pressure which led retention rate much lower.

In terms of industry, the CFO named retail, manufacturing, and transportation logistics as fastest-growing. Software and tech were the weakest.

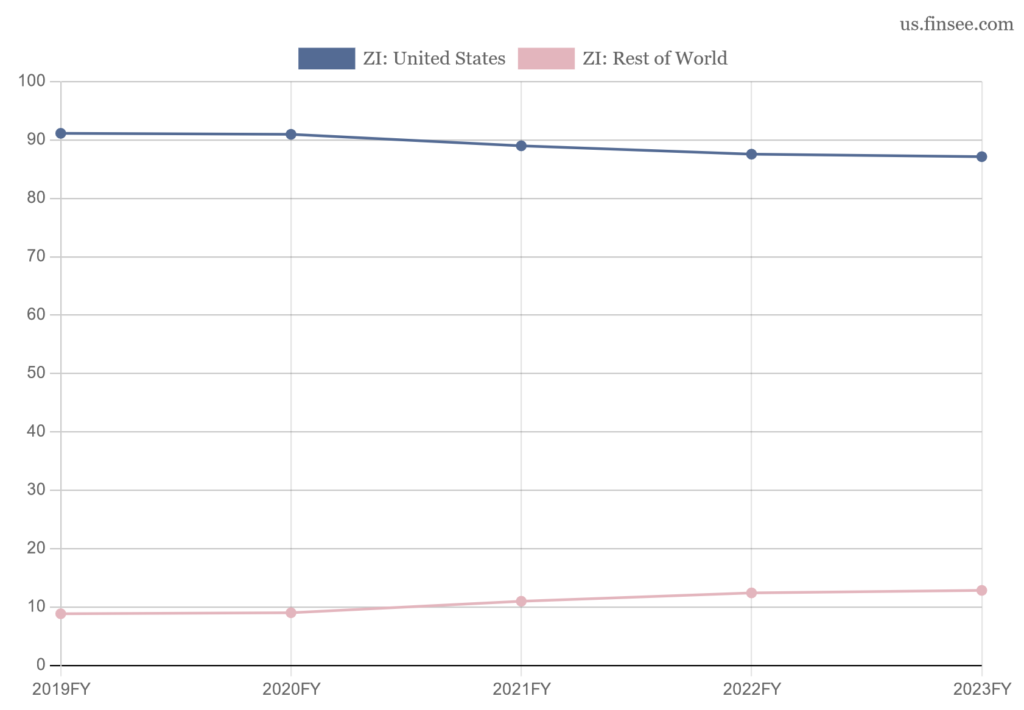

Revenue by geographic regions is dominated by the USA but international customers are slowly gaining more share. The chart shows percentages of total sales, which are reported once a year:

Profit and Loss

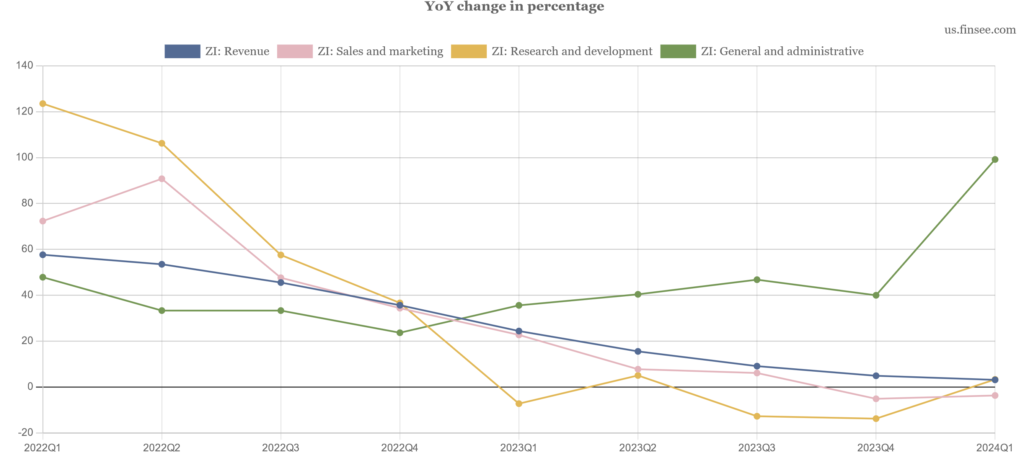

we expect sales growth to bottom in mid-2024 and start improving later this year with flattish operating income

The revenue retention rate continues to fall but the company expects it to stabilise and improve later this year as there are less contracts to renew. Previously Zoominfo reported retention rate once a year but in Q1 2024 they showed a quarterly number of 85%, calculated for the trailing twelve months, which was lower than a quarter earlier:

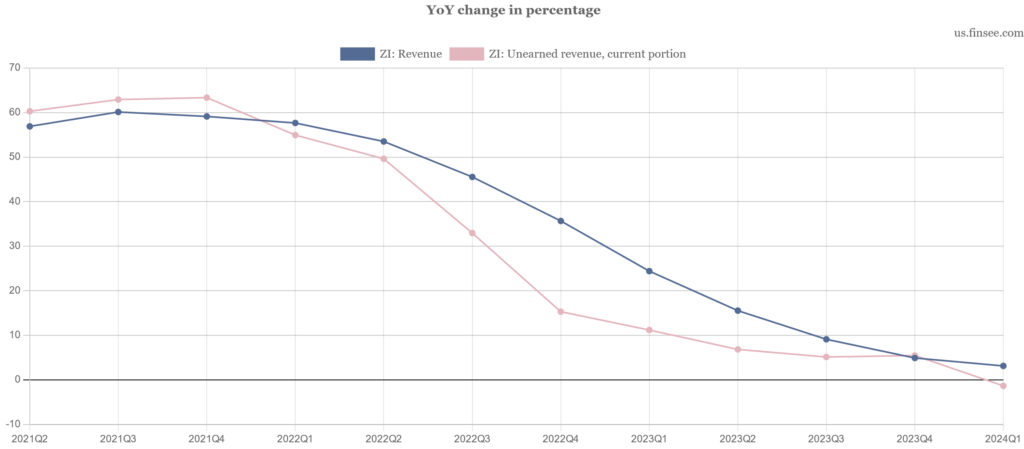

ZoomInfo’s sales growth slows down. Guidance for Q2 is for a slight decline of up to 1% YoY. 2024 full year guidance for revenue is to grow 1.3% – 2.5% YoY, which means sales will probably bottom in mid-2024 and start growing from there.

Unearned revenue (pre-payments from customers) decreased slightly YoY in Q1 2024, increasing the risk of declining sales for the next quarter or two:

Administrative expenses doubled year-on-year due to litigation settlement of $29.5M and a bit higher bad debt expense. Since this litigation is finished they should return to a more normalised level. Other operating expenses are moving in line with sales. Note that a small portion of R&D is capitalised: they grew a bit higher than the chart shows.

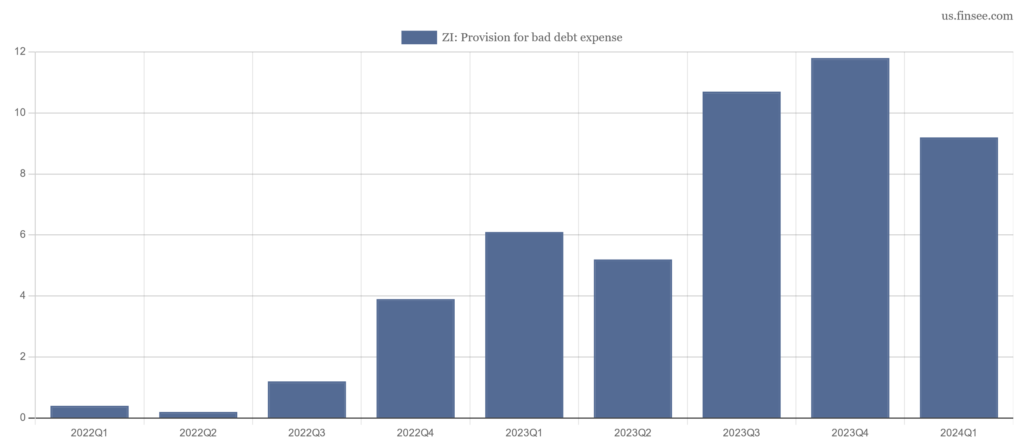

Provision for bad debt expense remains low at 3-4% of sales but it’s higher YoY with flat revenue. The company now requires more risky customers to pay by credit card or ACH, which improved the situation slightly in Q1 2024. Yet this is still a risk to watch:

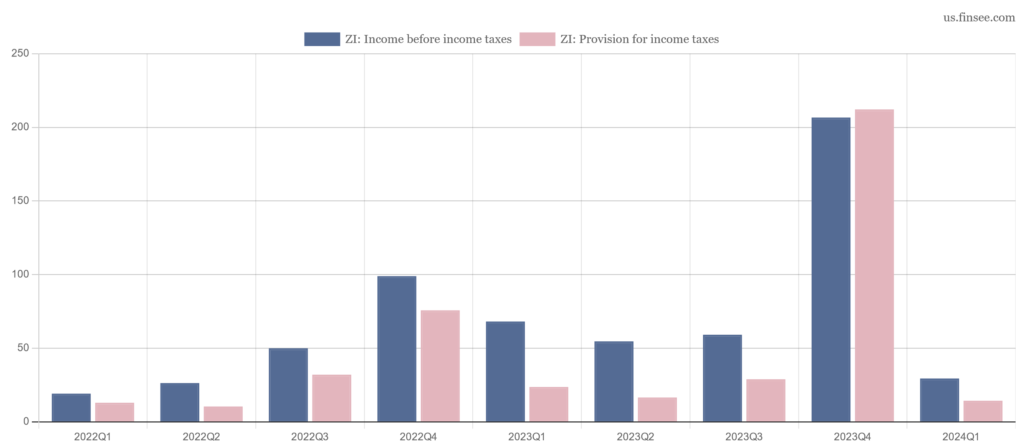

Net income was impacted by extremely high income taxes. ZoomInfo will pay them later but had to recognize them in 2022-23 Income statements. Explanation from the 2023 10-K report:

The effects of changes in state tax law and apportionment results in significant remeasurements of our state deferred tax assets. For the year ended December 31, 2023, the change mainly pertained to Massachusetts legislation enacted in the period which reduces the Company’s apportionment of income and loss to Massachusetts beginning in 2025. The change for the year ended December 31, 2022 principally pertained to movements in our geographical mix of sales, payroll and fixed assets among the states.

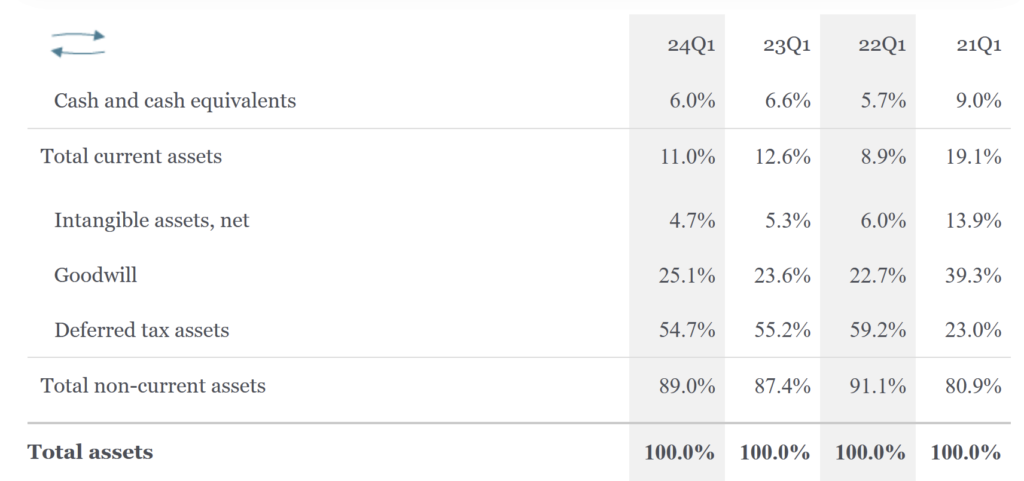

Balance sheet

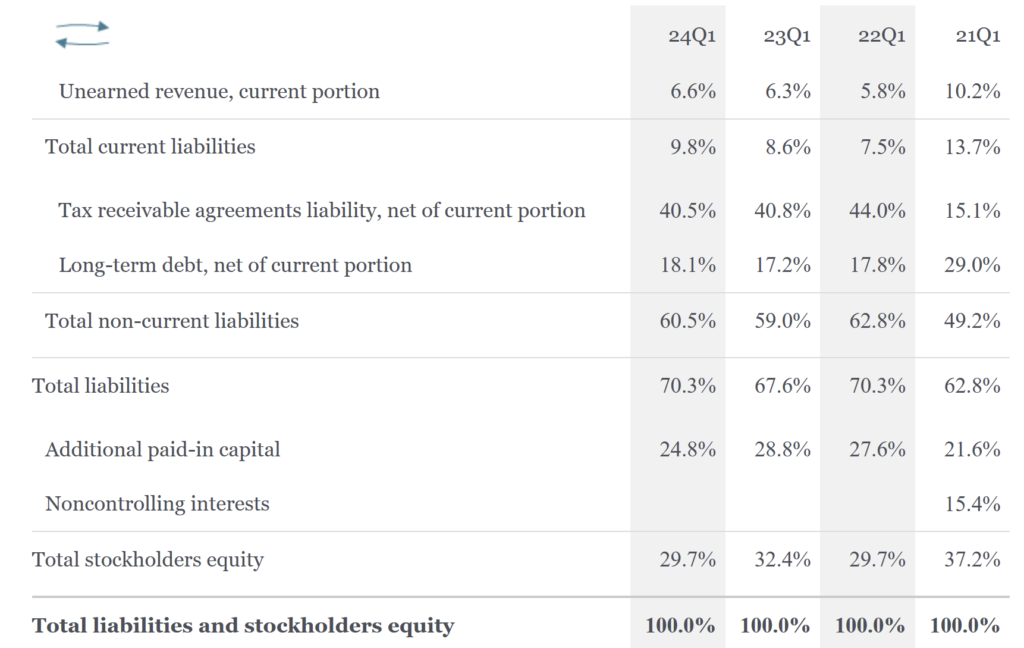

ZoomInfo has a huge amount of tax assets and liabilities on its balance sheet, with their values fluctuating when the laws change. Significant debt repayments are due in 2028, short-term liquidity is good

Tax receivable liability is 40.5% of total liabilities and equity. From 2023 10-K report:

ZoomInfo Intermediate Inc. is required to pay our Pre-IPO Owners for most of the benefits relating to any additional tax depreciation or amortization deductions that we may claim as a result of the ZoomInfo Tax Group’s allocable share of existing tax basis acquired in the IPO, the ZoomInfo Tax Group’s increase in its allocable share of existing tax basis, and anticipated tax basis adjustments the ZoomInfo Tax Group receives in connection with sales or exchanges of OpCo Units after the IPO, and certain other tax attributes.

ZoomInfo has $1.2B of debt, due in 2028. Principal payments during 2024-27 are $6M per year.

Current liabilities are only a small portion of the total and mostly consist of unearned revenue (prepayments from customers) which are usually fulfilled by providing services:

The same situation is on the assets side: the biggest item is deffered tax assets. Commentary from the 2023 10-K:

the Company had deferred tax assets of $3,795.5 million. These deferred tax assets consist primarily of $3,339.3 million of deductible temporary differences related to intangibles. The Company recognizes deferred tax assets to the extent it is more likely than not that the assets will be realized. The Company considered positive and negative evidence, including future reversals of existing taxable temporary differences, projected future taxable income, tax planning strategies, and recent results of operations.

Overall current assets are higher than current liabilities. Since cash is not needed to pay for unearned revenue, liquidity for the next 12 months is good.

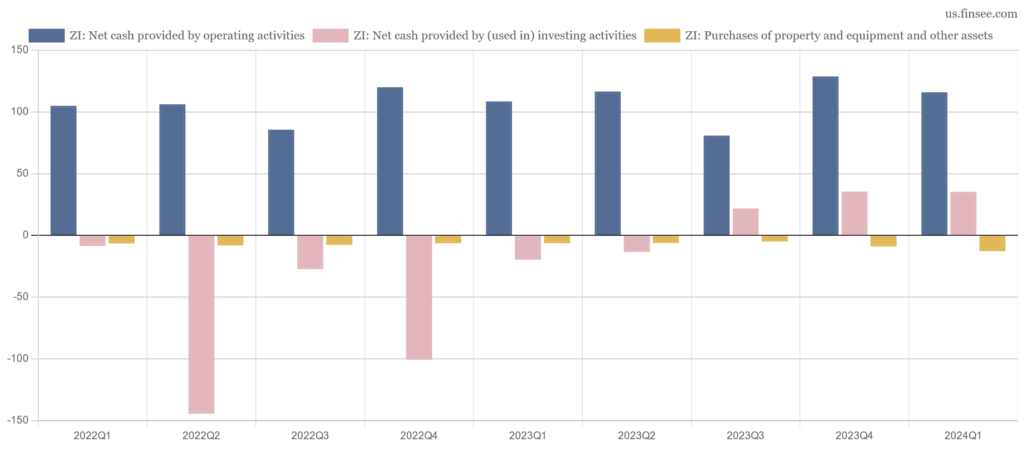

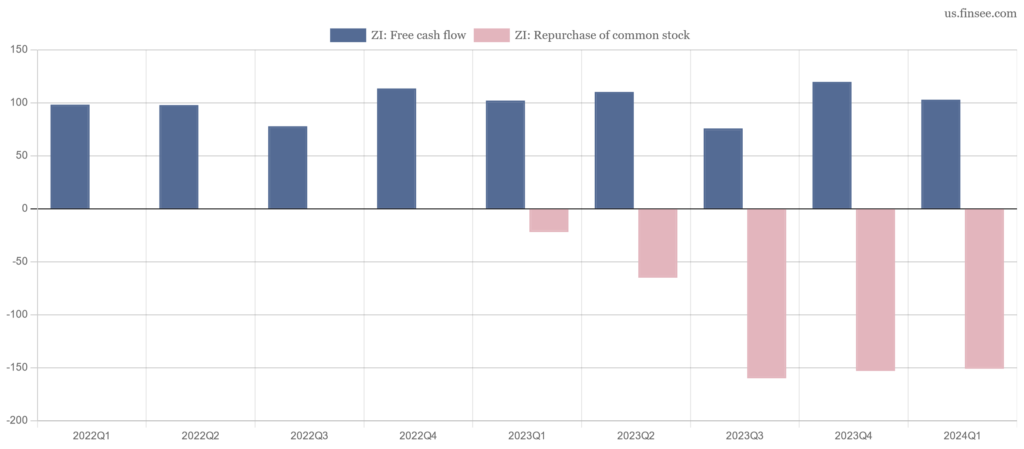

Cash Flow

ZoomInfo generates enough cash to cover its needs and repurchase shares

ZI receives $80-130M from operating activities per quarter. Positive investing cash flow during the last 3 quarters was the result of maturities of short-term investments.

Since purchases of property and equipment require only $5-13M per quarter, free cash flow allowed ZoomInfo to begin buybacks of its shares which accelerated recently as the stock price fell. ZI considers its shares very attractive with a forward PE of 13. During the last 4 quarters, the company bought back almost 8% of its shares, using also proceeds from investing cash flow:

Summary

There are a number of risks to watch for in the next quarterly reports:

- will customer feedback from AI Copilot be as positive as before?

- will retention rate, sales, and prepayments stop declining after Q2 2024?

- can the company decrease the provision for bad debt?

- will tax assets and liabilities remeasurements stop decreasing its net income?

We think the answer will be yes to all four questions at least after Q3 2024.

Forward PE 13 with huge possibilities for AI in ZoomInfo’s business make it a buy for us with a planned holding period of at least 12-18 months if things go according to the plan.